Chapter 7

Lessons from M&A Failures

"While the allure of a transformative merger can be strong, many M&A deals fail because companies overlook key factors such as cultural fit, realistic financial projections, and effective integration plans. Understanding the lessons from past failures is essential for building a robust M&A strategy that delivers value, rather than destroying it." — Sarah Jensen, Global Head of M&A Strategy, McKinsey & Company

Chapter 7 of Mastering Mergers and Acquisitions focuses on the critical lessons learned from M&A failures, examining common causes such as overvaluation, cultural clashes, and poor financial planning. The chapter explores both academic frameworks and industry best practices for identifying and mitigating risks in M&A transactions. By analyzing case studies from the digital and oil & gas industries, the chapter provides insights into how companies can avoid common pitfalls and develop more effective strategies for successful mergers. The chapter emphasizes the importance of learning from past failures to build sustainable M&A practices that contribute to long-term growth and profitability.

7.1. Understanding Failures in M&A

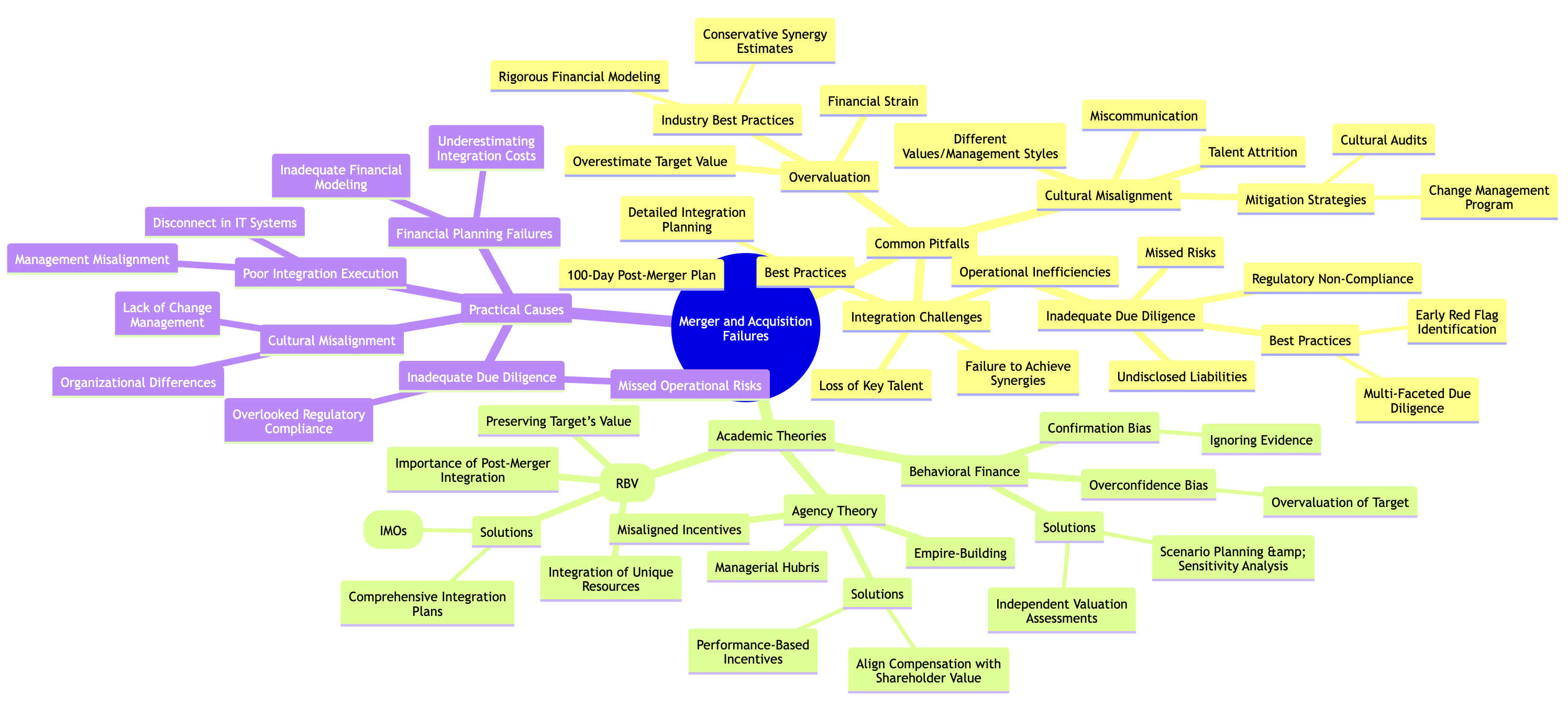

Mergers and acquisitions (M&A) are widely regarded as one of the most potent strategies for companies seeking growth, diversification, or a stronger competitive position. Yet, despite the promise of strategic synergies and financial benefits, M&A transactions often fail to achieve their intended outcomes. Research consistently shows that 50% to 70% of M&A deals underperform or fail, resulting in financial losses, operational disruption, and damage to the acquiring company’s long-term strategic goals. Understanding why these failures occur, and how to avoid them, requires a combination of academic insight and industry best practices. This exploration delves into the common pitfalls of M&A transactions, the academic theories that explain these failures, and how structured, strategic approaches can improve the odds of success.

Figure 7.1: Potential challenges on M&A failures.

Several academic frameworks provide a theoretical foundation for understanding the high failure rates in M&A. These theories shed light on the misaligned incentives, integration challenges, and behavioral biases that often contribute to M&A underperformance.

Agency theory suggests that misaligned incentives between the managers (agents) who execute M&A transactions and the shareholders (principals) who own the company often lead to poor decision-making. Managers may pursue deals that enhance their own power, prestige, or compensation, rather than deals that align with shareholder interests. This misalignment can result in overpayment for target companies, or acquisitions driven by empire-building rather than strategic value creation. Hubris, a key concept in agency theory, can lead to managers overestimating their ability to generate value from a deal, resulting in overly aggressive growth strategies that backfire. In practice, mitigating the risks posed by agency theory requires aligning executive compensation with long-term shareholder value. Performance-based incentives that focus on post-merger success, rather than just the completion of the deal, can help ensure that M&A strategies are driven by shareholder interests rather than managerial ego.

The resource-based view (RBV) of the firm emphasizes the importance of unique, valuable, and inimitable resources in generating sustainable competitive advantage. From an M&A perspective, RBV highlights the importance of successfully integrating the target company’s resources—such as technology, intellectual property, and human capital—into the acquiring company’s operations. Failure to do so often leads to the erosion of the target’s value post-acquisition. For example, if the acquirer cannot effectively leverage the target’s proprietary technology or retain key talent, the expected synergies from the deal may never materialize. Post-merger integration is critical to preserving and enhancing the target company’s value. In practice, companies must develop comprehensive integration plans that ensure smooth coordination across departments, IT systems, supply chains, and corporate cultures. Integration management offices (IMOs) are commonly used in industry to oversee this process, with dedicated teams ensuring that the key resources acquired are successfully integrated to achieve long-term strategic objectives.

Behavioral finance offers additional insights into M&A failures by highlighting the cognitive biases that influence decision-making. Overconfidence bias is particularly prevalent in M&A transactions, where acquirers often overestimate their ability to generate value from the deal and underestimate the risks involved. This overconfidence leads to overvaluation of the target company, as acquirers convince themselves that the potential synergies will justify paying a premium. In reality, many of these synergies fail to materialize, and the acquirer ends up absorbing a target that is worth far less than anticipated. Another cognitive bias is the confirmation bias, where decision-makers selectively focus on information that supports the deal, while ignoring or downplaying evidence that suggests the acquisition may be risky. This skewed perception often leads to flawed decisions, resulting in poor deal execution. To counteract these biases, companies can implement independent valuation assessments and use third-party advisors to provide objective analyses. Rigorous scenario planning and sensitivity analysis can help acquirers prepare for different post-merger outcomes, ensuring that decisions are grounded in reality rather than overconfidence or selective perception.

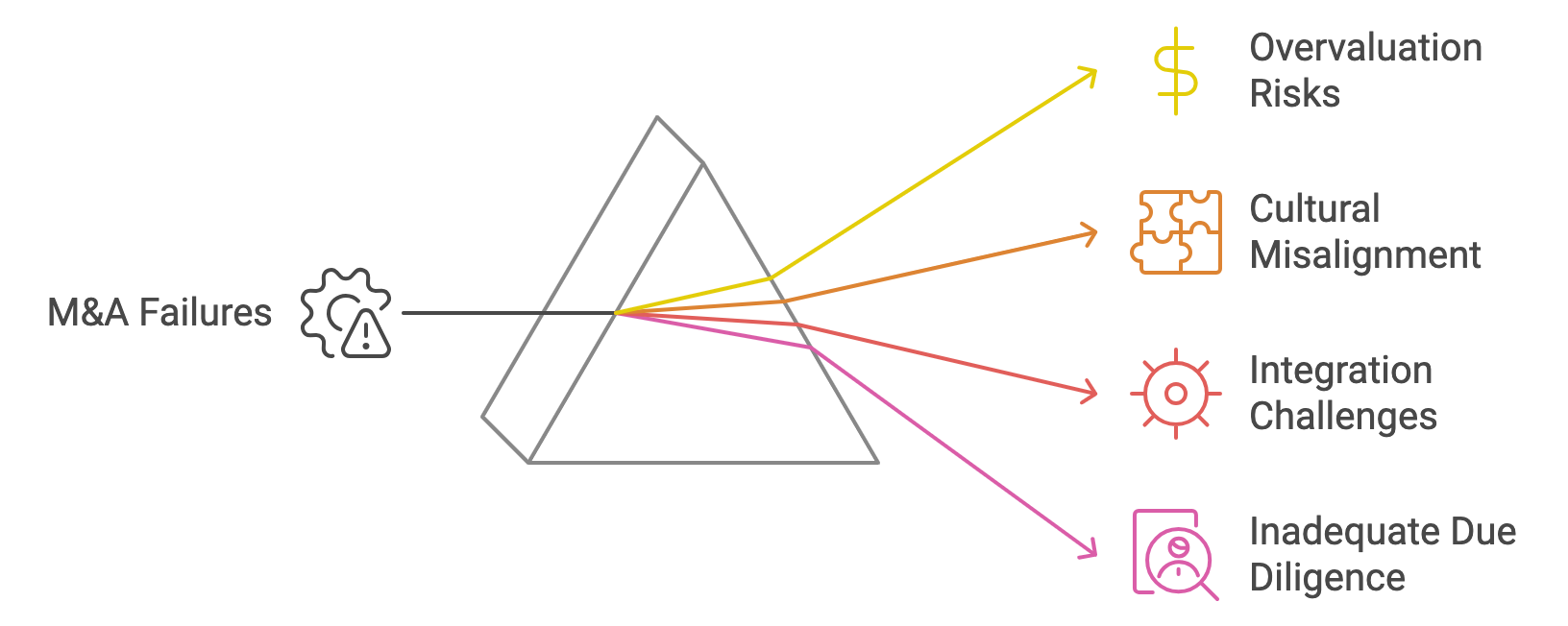

While academic theories provide the conceptual framework, the practical causes of M&A failures typically revolve around several key issues. These failures are often interrelated, amplifying each other’s effects and contributing to the overall breakdown of the deal.

Figure 7.2: Common issues in M&A failure.

One of the most common causes of M&A failure is overvaluation. Acquirers frequently overestimate the target’s future earnings potential or the value of anticipated synergies. This leads to paying a premium for the target, often resulting in financial strain when expected returns fail to materialize. Inadequate financial planning can compound this issue, as companies underestimate the costs associated with integration, such as restructuring, technology upgrades, or cultural realignment. Best practice in the industry involves conducting rigorous financial modeling during the due diligence phase. This includes detailed assessments of the target’s financial health, stress-testing future projections, and developing conservative synergy estimates. Using discounted cash flow (DCF) models, comparative company analysis (CCA), and precedent transaction analysis ensures that valuations are grounded in sound financial principles, helping to avoid overpayment.

Cultural misalignment is another major contributor to M&A failure. Research shows that up to 30% of mergers fail due to cultural clashes, particularly when the acquiring and target companies have fundamentally different values, management styles, or organizational structures. Cultural incompatibility can lead to miscommunication, low morale, talent attrition, and a failure to integrate business practices effectively. Addressing cultural differences early through cultural audits and organizational assessments is essential for mitigating these risks. Companies should not only assess the operational and strategic fit of the target but also determine how well the corporate cultures align. A robust change management program, driven by leadership from both companies, can help bridge cultural gaps and ensure a smooth integration.

Integration challenges are among the most significant reasons for M&A underperformance. Poorly executed integration can lead to operational inefficiencies, loss of key talent, and failure to achieve synergies. Common integration failures include the inability to merge IT systems, disconnects between management teams, and lack of alignment on product development or market strategy. Successful M&A transactions rely on detailed integration planning from the outset. This includes setting clear integration goals, appointing dedicated integration teams, and establishing a timeline for integrating core functions such as finance, HR, and IT. Industry best practices suggest that companies should develop a 100-day post-merger plan, ensuring that immediate integration priorities are addressed without disrupting ongoing operations.

Inadequate due diligence can lead to the acquirer overlooking critical risks, such as undisclosed liabilities, regulatory non-compliance, or operational weaknesses. Insufficient due diligence leaves the acquirer vulnerable to unexpected issues that can erode the value of the deal. For example, acquiring a company with unresolved legal disputes or pending regulatory investigations can result in costly penalties or operational delays. Industry best practices involve a multi-faceted due diligence process that covers financial, legal, operational, and cultural dimensions. This approach helps identify red flags early in the transaction and allows the acquirer to develop strategies for mitigating these risks.

Several high-profile M&A failures provide valuable lessons for companies considering acquisitions. Case studies from industries such as technology, telecommunications, and retail demonstrate the importance of strategic alignment, cultural integration, and realistic financial expectations.

Daimler-Chrysler Merger (1998): This merger is a classic example of cultural incompatibility. The German engineering culture of Daimler clashed with the more relaxed, entrepreneurial culture of Chrysler, leading to management conflicts, talent attrition, and eventual failure of the merger. The lesson: Cultural alignment is critical to post-merger success.

AOL-Time Warner Merger (2000): This merger failed largely due to overvaluation and misalignment of strategic goals. AOL’s overestimation of synergies, combined with cultural and operational integration issues, led to one of the most significant M&A failures in history. The lesson: Financial discipline and realistic synergy estimates are essential.

HP’s Acquisition of Autonomy (2011): HP’s acquisition of Autonomy failed due to inadequate due diligence and overvaluation. HP later wrote down $8.8 billion of the deal’s value, citing accounting irregularities and misrepresentation by Autonomy. The lesson: Thorough and independent due diligence is non-negotiable.

M&A transactions offer substantial potential for growth, diversification, and competitive advantage, but they are fraught with risks that must be carefully managed. By combining academic insights from agency theory, resource-based view (RBV), and behavioral finance with industry best practices such as rigorous financial modeling, cultural audits, and detailed integration planning, companies can significantly increase their chances of M&A success.

A strategic, robust, and comprehensive approach to M&A involves not only identifying the right targets but also ensuring that every aspect of the transaction—from valuation and due diligence to integration and cultural alignment—is executed with precision. Learning from past failures and applying structured methodologies can help acquirers avoid common pitfalls, ensuring that their M&A deals deliver the expected financial and strategic benefits.

7.2. Lessons from M&A Failures

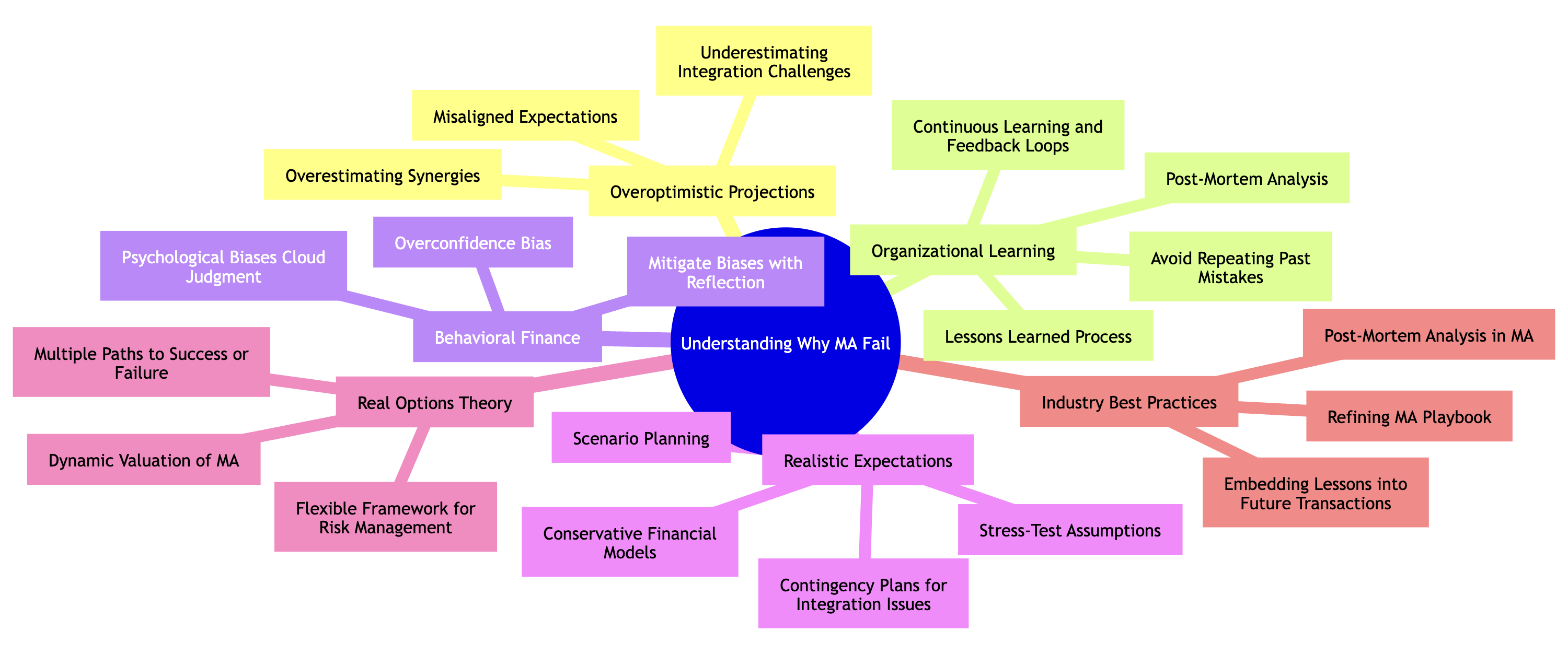

Understanding why mergers and acquisitions (M&A) fail is not just about hindsight; it is crucial for developing strategic, robust, and comprehensive frameworks that lead to successful outcomes. M&A failures often result from overoptimistic projections, poor integration planning, and underestimating challenges. Companies can mitigate these risks by combining academic insights on organizational learning with industry best practices that emphasize preparation, realistic expectations, and a structured approach to analyzing past failures.

The concept of organizational learning is particularly relevant to understanding and improving M&A outcomes. Organizational learning theory posits that organizations evolve and improve by systematically analyzing their past experiences—both successes and failures. In the context of M&A, companies that reflect on previous failures and extract key lessons are better positioned to avoid repeating the same mistakes.

This reflective learning process is often referred to as a "lessons learned" analysis or post-mortem. According to organizational learning theory, companies that fail to engage in this process are at greater risk of making cognitive errors or strategic missteps in future transactions. By contrast, organizations that adopt continuous learning and feedback loops are better equipped to refine their M&A strategies, ensuring that each transaction builds on the lessons of the past.

Figure 7.3: Understanding why M&A failed.

Moreover, behavioral finance concepts—such as overconfidence bias—often explain why acquirers enter M&A deals with overly optimistic expectations of synergies, cost savings, or revenue growth. These psychological biases can cloud judgment, leading decision-makers to overlook potential risks or underestimate the complexities of integrating the target company. Organizational learning helps mitigate these biases by fostering a culture of critical reflection, ensuring that past failures are used as a tool for improvement rather than dismissed as anomalies.

One of the most valuable lessons from failed M&A transactions is the need for realistic expectations. Companies often approach deals with overly optimistic projections of synergies, cost savings, or revenue growth. However, academic research and industry data consistently show that achieving these synergies is often far more difficult and time-consuming than anticipated. For example, cost synergies from merging operational functions, such as finance or procurement, may take years to materialize due to complexities in integrating systems, processes, or cultures.

To counter these challenges, companies need to stress-test their assumptions and develop more conservative financial models during the pre-deal phase. This includes evaluating best-case, worst-case, and most-likely-case scenarios to ensure that the projected synergies are achievable. Additionally, firms should build in contingency plans for addressing common integration issues, such as cultural conflicts, IT system incompatibilities, or supply chain disruptions.

One academic framework relevant here is the real options theory, which views M&A as a series of strategic investments that unfold over time. The value of the deal is not fully realized at the closing but depends on future decisions, adjustments, and successful integration. By adopting this mindset, companies can move away from a single-point valuation based on overoptimistic synergies and instead view the acquisition as a dynamic process with multiple paths to success or failure. This provides a more flexible framework for managing risk and adjusting strategy post-acquisition.

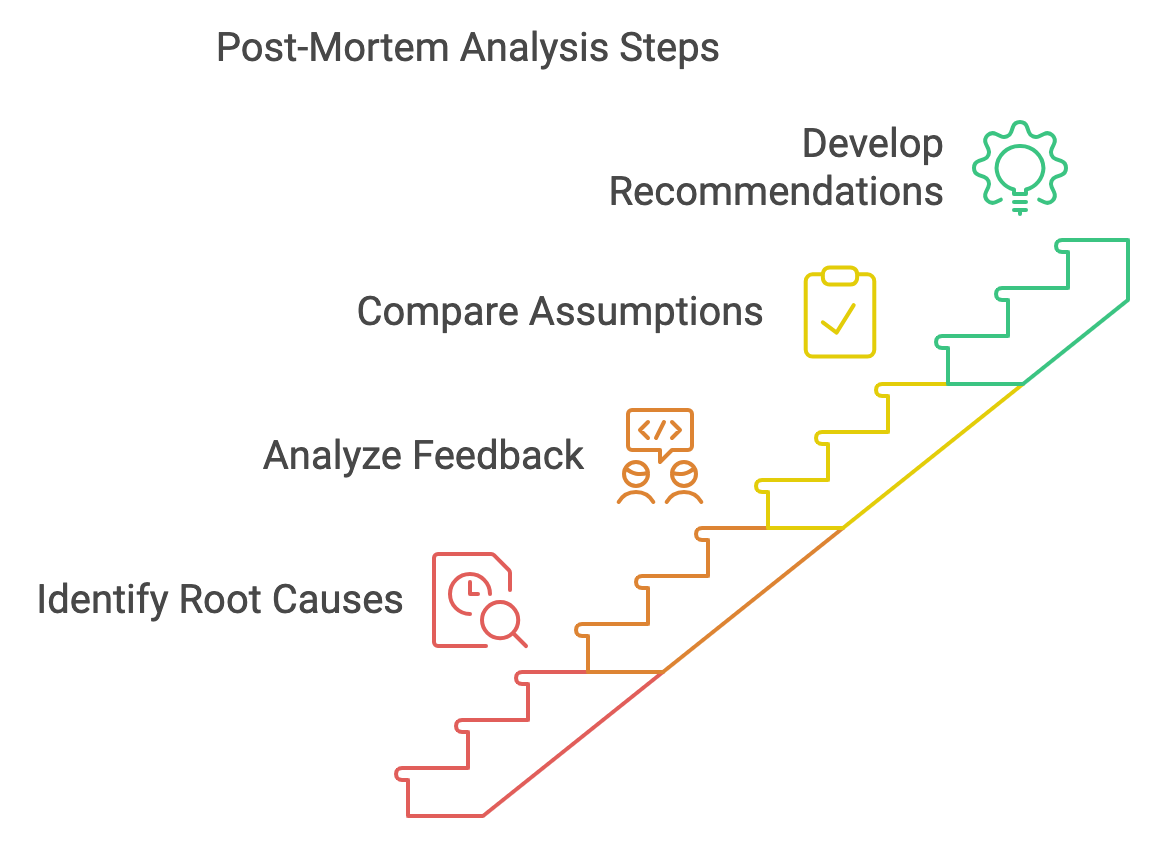

In industry, post-mortem analyses are a critical component of improving M&A performance. Companies that conduct in-depth reviews of failed transactions gain insights into what went wrong, why it happened, and how similar issues can be avoided in the future. These analyses are not merely retrospective; they are forward-looking exercises aimed at refining the company’s M&A playbook and embedding lessons into future transactions.

Figure 7.4: Post-mortem analysis steps in M&A failure.

A well-executed post-mortem analysis includes several key steps:

Identifying the Root Causes: This involves a deep dive into the specific factors that contributed to the failure of the deal. For example, did the acquirer overpay due to poor financial modeling? Was the integration plan too ambitious? Were there hidden legal or regulatory risks that were not fully understood during due diligence?

Analyzing Stakeholder Feedback: Gathering insights from various stakeholders—such as employees, investors, and customers—can provide a holistic view of what went wrong. For instance, employees might highlight cultural mismatches, while investors may point to financial miscalculations.

Comparing Assumptions vs. Reality: By comparing the initial assumptions made during the pre-deal phase (e.g., expected synergies, growth projections) with the actual outcomes, companies can identify where their expectations diverged from reality.

Developing Actionable Recommendations: The final step is to distill the insights from the post-mortem analysis into actionable recommendations that can inform future M&A strategy. These recommendations should focus on improving due diligence, refining financial models, and adjusting integration plans to be more realistic and achievable.

By embedding these lessons into their M&A frameworks, companies create playbooks that outline both the critical success factors and potential pitfalls of deals. These playbooks serve as a reference guide for decision-makers, helping them navigate future transactions more effectively. For example, a playbook might highlight the need for greater cultural due diligence in industries where organizational culture is a key driver of success, or it might emphasize the importance of integration planning for tech-heavy acquisitions where system compatibility is essential.

Examining real-world case studies of failed M&A transactions offers practical insights into how companies can learn from their mistakes and develop stronger strategies. Each failure provides a unique lesson that can be applied to future deals, demonstrating the value of post-mortem analyses and organizational learning.

HP’s Acquisition of Autonomy (2011): HP’s $11 billion acquisition of Autonomy is widely regarded as one of the most significant M&A failures in recent history. The deal failed due to overvaluation, inadequate due diligence, and alleged financial misrepresentation by Autonomy. HP later wrote down the value of the acquisition by $8.8 billion. The key lesson here is the importance of rigorous due diligence and the need for independent verification of financial data before finalizing a deal. Post-mortem analysis could have highlighted the red flags that were missed in the early stages of due diligence.

Daimler’s Acquisition of Chrysler (1998): Daimler’s merger with Chrysler was hailed as a strategic move to create a global automotive giant. However, the merger ultimately failed due to cultural clashes and misaligned strategic goals between the two companies. Daimler’s German management style did not mesh well with Chrysler’s more laid-back, American corporate culture, leading to significant friction. The lesson from this failure is the importance of conducting cultural audits and ensuring that both companies share a compatible vision and values. This case highlights the need for post-merger integration planning that prioritizes cultural alignment.

AOL-Time Warner Merger (2000): The AOL-Time Warner merger, valued at $165 billion, is another high-profile M&A failure. The deal was driven by overly optimistic synergies between AOL’s online platform and Time Warner’s media assets, but these synergies never materialized. The companies struggled with integration, and the combined entity faced significant operational inefficiencies. The key lesson here is that synergies should be realistically modeled and tested against real-world conditions, rather than relying on abstract projections.

To improve future M&A outcomes, companies should take the insights from post-mortem analyses and case studies and embed them into their M&A playbooks. These playbooks serve as strategic guides, ensuring that the lessons from past failures are institutionalized and inform future decision-making. A comprehensive M&A playbook includes:

Detailed Pre-Deal Checklists: Outlining the key steps and considerations for conducting due diligence, including financial, legal, operational, and cultural assessments.

Realistic Synergy Projections: Providing guidelines for modeling synergies and emphasizing the need for conservative estimates based on real-world data, rather than overly optimistic projections.

Cultural Integration Strategies: Offering templates for conducting cultural audits and strategies for aligning organizational cultures during the post-merger integration phase.

Post-Integration Metrics: Defining clear metrics for assessing the success of the integration process, such as employee retention rates, system compatibility, and operational efficiencies.

Contingency Plans: Highlighting common post-deal risks, such as customer attrition, supply chain disruptions, or regulatory challenges, and providing strategies for mitigating these risks.

By institutionalizing these lessons into playbooks, companies create a living document that evolves with each transaction. This ensures that the entire organization benefits from past experiences and approaches future M&A deals with a clear, strategic framework that improves the likelihood of success.

To improve the success rate of M&A transactions, companies must embrace a strategic, robust, and comprehensive approach that incorporates both academic insights and industry best practices. Organizational learning and post-mortem analyses are essential tools for identifying the root causes of failure and embedding these lessons into future deals. By focusing on realistic expectations, detailed preparation, and cultural alignment, companies can significantly increase their chances of executing successful transactions that deliver long-term value.

A structured M&A playbook that integrates lessons learned from past failures ensures that companies approach each deal with a well-defined strategy. This, combined with rigorous due diligence, conservative financial modeling, and effective post-merger integration planning, provides a solid foundation for M&A success, transforming past failures into future opportunities for growth and sustainability.

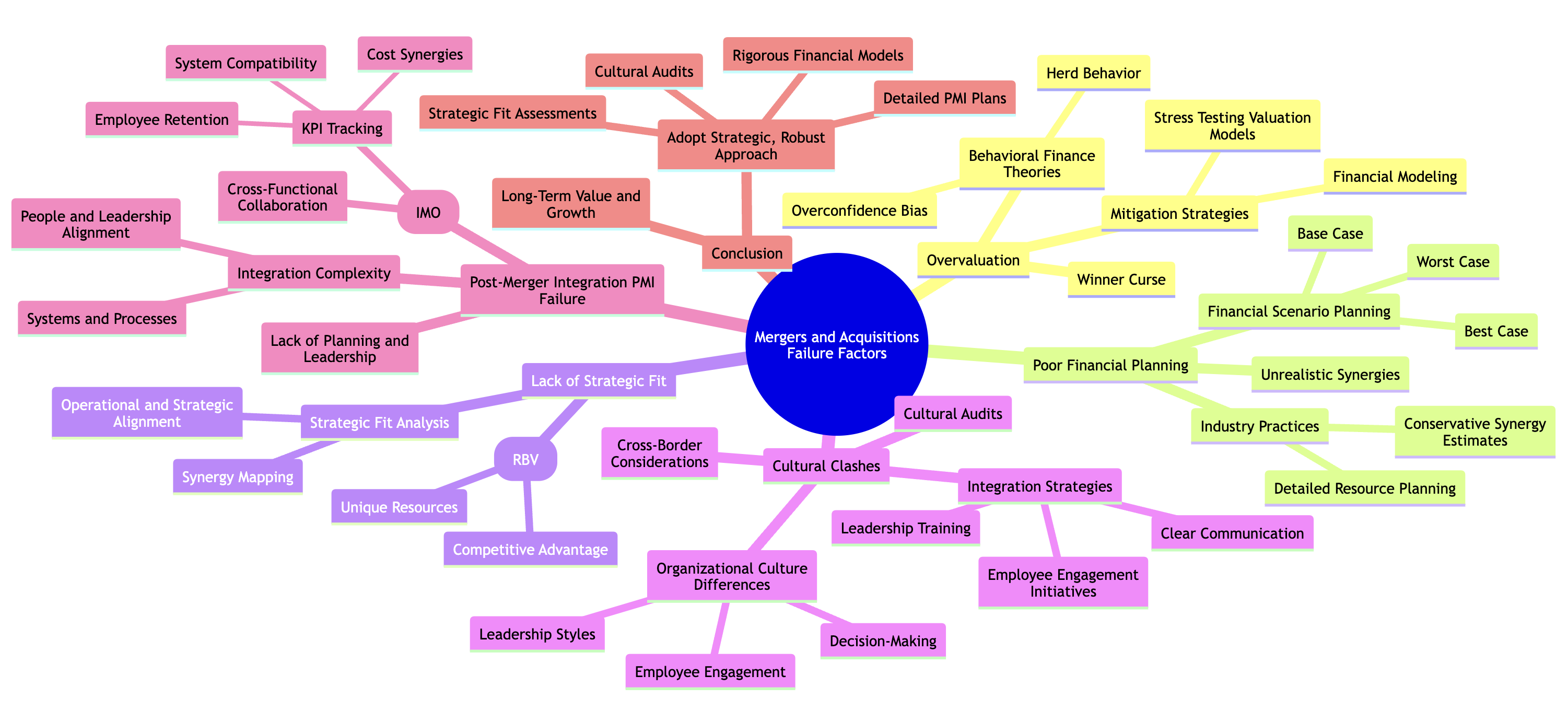

7.3. Common Causes of Unsuccessful Mergers

Mergers and acquisitions (M&A) are complex strategic transactions that hold significant potential for growth, diversification, and competitive advantage. However, academic research and industry experience reveal that many M&A deals fail to meet expectations, often due to a combination of recurring factors such as overvaluation, poor financial planning, lack of strategic fit, cultural clashes, and failure in post-merger integration (PMI). These causes of failure are not isolated; they frequently overlap, compounding the challenges and leading to underperformance. By examining each of these factors from both academic frameworks and industry best practices, companies can better understand the underlying risks and develop more robust strategies to avoid these pitfalls.

Figure 7.5: Common factors that make M&A failed.

Overvaluation is one of the most common causes of M&A failure. It occurs when the acquiring company overestimates the value of the target and pays a price that cannot be justified by future earnings or synergies. Academically, overvaluation can be explained by the concept of the winner’s curse, which posits that in competitive bidding scenarios, the acquirer often overpays due to the pressure to outbid competitors. This overpayment typically leads to lower returns on investment post-acquisition.

The issue of overvaluation is further illuminated by behavioral finance theories such as overconfidence bias and herd behavior. Overconfidence bias leads acquirers to believe they can extract more value from the deal than is realistically possible, often underestimating the risks or complexities involved. Herd behavior occurs when companies pursue acquisitions because their peers are doing the same, which can create market hype and drive up valuations beyond rational levels.

Industry best practices attempt to mitigate these biases through rigorous financial modeling techniques, such as discounted cash flow (DCF) analysis, comparable company analysis (CCA), and precedent transaction analysis. These methods are designed to provide a data-driven approach to valuation, but they are only as reliable as the assumptions behind them. If the assumptions regarding projected revenue growth, cost savings, or synergies are overly optimistic or based on flawed data, even the most sophisticated models can lead to overvaluation. Thus, a strategic approach involves conducting stress tests on valuation models and considering a range of market conditions to avoid paying a premium that cannot be recovered.

Poor financial planning is another critical factor that contributes to M&A failure. It often manifests in unrealistic expectations about the cost of integration, overestimated synergies, or failure to account for market volatility. Inadequate financial planning leads to financial strain post-merger, as acquirers are unable to meet the costs associated with integration or the expected benefits fail to materialize.

From an academic standpoint, financial planning should incorporate scenario planning and sensitivity analysis to model multiple potential outcomes. Theories of financial risk management stress the importance of developing various financial scenarios, such as best case, base case, and worst case, to better prepare for different market conditions and integration challenges.

In industry practice, the emphasis is on detailed resource planning for post-merger integration. This includes assessing not only the direct financial outlay required to complete the transaction but also the costs associated with integrating IT systems, supply chains, workforces, and corporate cultures. Additionally, many M&A deals fail because acquirers overestimate synergies, particularly in cost-cutting, revenue enhancement, or market expansion. To avoid this, industry experts recommend adopting conservative synergy estimates and factoring in potential integration risks that could erode these benefits.

A lack of strategic fit between the acquirer and the target is a fundamental reason why many M&A transactions fail. The resource-based view (RBV), a prominent theory in strategic management, argues that acquisitions are most successful when they enhance the acquirer’s competitive advantage through the acquisition of unique and valuable resources. For example, acquiring a company with superior technology, intellectual property, or a strong customer base can provide a strategic boost to the acquiring firm.

However, many M&A deals are driven by short-term financial gains or external pressures, rather than a clear strategic alignment. When there is no clear connection between the target’s operations, market position, or capabilities and the acquirer’s long-term objectives, the acquisition is unlikely to deliver sustained value.

In industry practice, companies must conduct a rigorous strategic fit analysis during the due diligence phase to assess whether the target aligns with the acquirer’s goals. This involves evaluating the target’s core competencies, customer segments, market position, and operational processes to determine how well they complement the acquirer’s existing business model. A comprehensive synergy mapping exercise, where the potential value drivers of the target are compared against the acquirer’s objectives, can help identify whether the acquisition makes strategic sense. Without this alignment, the deal is likely to result in operational inefficiencies, unmet expectations, and ultimately, value destruction.

Cultural clashes are a pervasive and often underestimated cause of M&A failure. Organizational culture refers to the shared values, behaviors, and practices that define how work is done within a company. When two companies with differing cultures attempt to merge, conflicts can arise in areas such as decision-making, leadership styles, and employee engagement. These differences can lead to friction, low morale, and even the departure of key talent, undermining the value of the acquisition.

Academically, cultural integration is explored through organizational behavior and change management theories, which emphasize the need for leadership alignment, effective communication, and employee involvement during the integration process. Research consistently shows that M&A deals are more successful when the acquiring company actively manages cultural differences, rather than assuming that the target will simply adapt to the acquirer’s way of doing things.

Industry experts recommend conducting cultural audits during the due diligence phase to identify potential areas of conflict. This involves assessing the values, norms, and practices of both organizations to determine whether they are compatible. If cultural differences are identified, companies must develop integration strategies that address these challenges proactively. This can include leadership training, employee engagement initiatives, and clear communication plans that outline how the merged company will operate on a day-to-day basis. For cross-border transactions, where cultural differences may be even more pronounced, the importance of cultural alignment becomes even greater.

Even when the financial and strategic rationale for a deal is sound, many M&A transactions fail because of poor post-merger integration (PMI). Integration is often the most complex and challenging phase of an M&A transaction, as it involves aligning not only systems and processes but also people, cultures, and leadership styles.

In academic literature, PMI failures are often attributed to inadequate planning and lack of leadership. Research on integration management suggests that successful PMI requires cross-functional collaboration, clear objectives, and dedicated leadership from both the acquirer and the target. Without a well-defined integration plan, companies are likely to face operational disruptions, loss of key talent, and failure to achieve synergies.

In industry practice, PMI is often managed through the establishment of an Integration Management Office (IMO), which oversees the coordination of all integration activities. The IMO is responsible for ensuring that integration objectives are met, that there is alignment between the two companies’ operations, and that any issues are addressed quickly and efficiently. Key performance indicators (KPIs) are also used to track the success of the integration process, such as employee retention rates, system compatibility, and cost synergies achieved.

The importance of PMI cannot be overstated, as it is often the phase where the value of the deal is either realized or lost. Companies that invest in a thorough and strategic integration plan, with dedicated resources and leadership, are far more likely to succeed in achieving their M&A objectives.

The causes of M&A failure are diverse, but they often stem from overvaluation, poor financial planning, lack of strategic fit, cultural clashes, and failure to achieve post-merger integration. Each of these factors can derail a deal on its own, but they frequently occur in combination, compounding the risks and challenges.

To avoid these pitfalls, companies must adopt a strategic, robust, and comprehensive approach to M&A. This includes using rigorous financial models with conservative assumptions, conducting strategic fit assessments, implementing cultural audits, and developing detailed post-merger integration plans. By learning from both academic insights and industry best practices, companies can improve their chances of executing successful M&A transactions that create long-term value and growth.

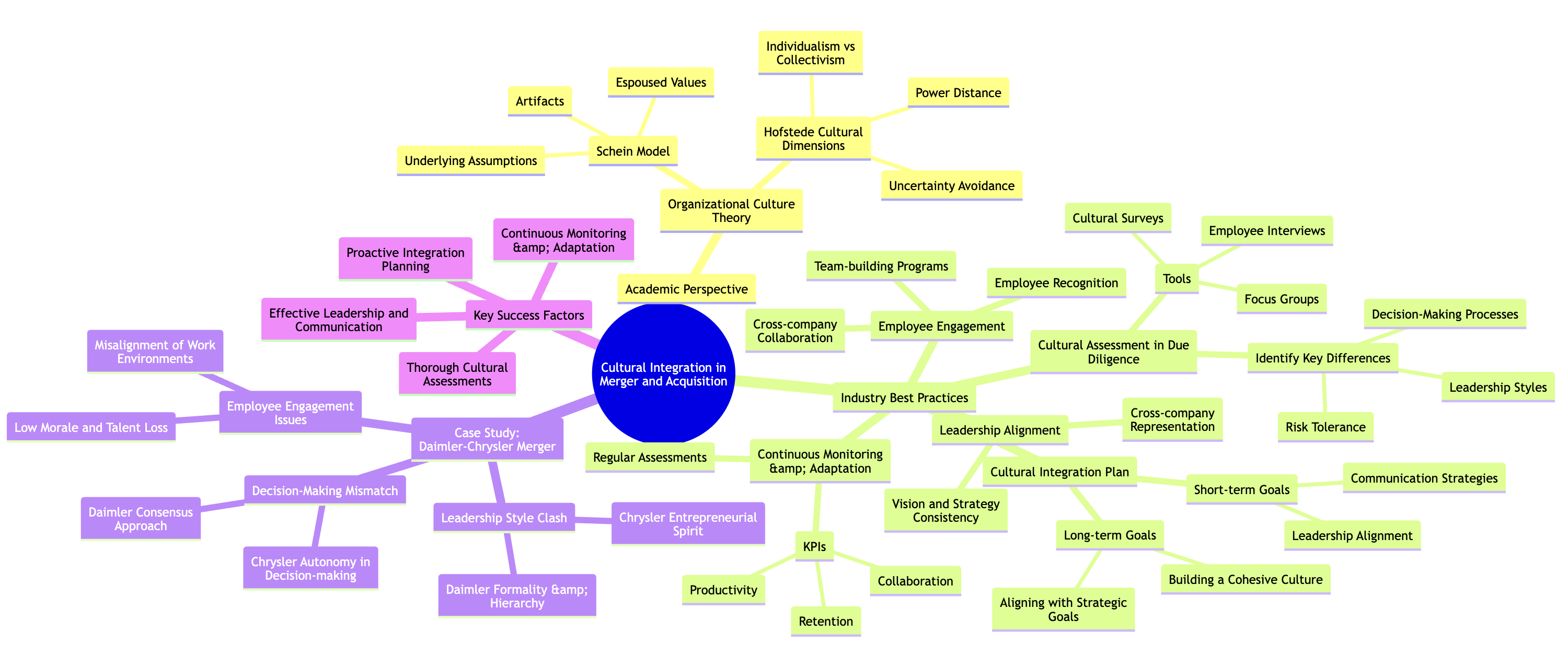

7.4. Cultural Clashes and Integration Issues

Cultural integration is widely recognized as one of the most difficult and critical aspects of post-merger integration (PMI). When two companies with distinct corporate cultures merge, the potential for friction, misalignment, and even failure is significantly heightened. This is especially true in cross-border M&A, where national cultural differences compound the complexities of organizational integration. A strategic, robust, and comprehensive approach to cultural integration is necessary to prevent these issues from undermining the potential value of the merger.

From an academic perspective, successful cultural integration in M&A is grounded in a deep understanding of both organizations’ cultures and how they align—or conflict. Organizational culture theory emphasizes that culture is not just about surface-level behaviors or visible artifacts but includes deeper values, assumptions, and norms that guide how employees interact, make decisions, and approach work. Academic research shows that failing to account for these underlying cultural differences can lead to significant integration challenges, including reduced productivity, increased turnover, and missed synergies.

Figure 7.6: Common cultural and integration clashes that make M&A failed.

One of the most relevant academic frameworks for understanding cultural integration is Edgar Schein's model of organizational culture, which divides culture into three levels: artifacts, espoused values, and underlying assumptions. Effective cultural integration requires addressing each of these levels, starting with visible practices and policies (artifacts) and extending to the more deeply ingrained values and assumptions that shape employee behavior. Schein’s framework helps explain why superficial integration efforts, such as aligning corporate branding or reorganizing teams, often fail if the deeper, less visible aspects of culture are not addressed.

Another key academic insight comes from Geert Hofstede's cultural dimensions theory, which highlights how national culture affects organizational behavior. In cross-border M&A, differences in power distance, individualism versus collectivism, and uncertainty avoidance can significantly affect leadership styles, decision-making processes, and employee interactions. These national cultural differences must be carefully managed to avoid conflict and promote collaboration across the merged entity.

A classic and frequently cited example of cultural clashes leading to M&A failure is the 1998 merger between Daimler-Benz and Chrysler, which underscores the importance of cultural alignment. The merger, valued at $36 billion, was heralded as a strategic move to combine Daimler’s engineering prowess with Chrysler’s more innovative and agile approach. However, significant differences in the German and American corporate cultures derailed the potential for synergies.

Leadership Style: Daimler-Benz’s German management emphasized formality, hierarchy, and long-term planning, while Chrysler’s leadership was known for a more informal, entrepreneurial, and risk-taking culture. The clash in leadership styles led to conflicting management decisions, miscommunication, and growing dissatisfaction among Chrysler employees, who felt stifled by Daimler’s more rigid approach.

Decision-Making Processes: In Daimler’s German corporate culture, decision-making was characterized by a methodical, consensus-driven approach, while Chrysler’s American culture favored rapid decision-making and greater autonomy for managers. This mismatch in decision-making processes slowed down operations, created bottlenecks, and reduced the effectiveness of collaboration between teams.

Employee Engagement: The cultural differences also affected employee engagement and morale. Chrysler employees struggled to adapt to Daimler’s more structured environment, and many key employees left the company, leading to a loss of talent and institutional knowledge.

By 2007, Daimler sold Chrysler at a significant loss, demonstrating how cultural clashes can severely undermine the strategic objectives of an M&A transaction. The case highlights the need for cultural due diligence and an intentional approach to managing cultural integration.

Industry best practices for managing cultural integration emphasize the need for a structured, proactive approach that begins during the due diligence phase and continues throughout the PMI process. Successfully managing cultural integration involves several key steps:

A thorough cultural assessment during due diligence is essential for identifying potential areas of conflict or misalignment between the two organizations. This involves analyzing the organizational values, leadership styles, communication norms, and decision-making processes of both companies. Tools such as cultural surveys, employee interviews, and focus groups can provide valuable insights into the cultural DNA of both organizations. In cross-border deals, understanding national cultural differences, as outlined by Hofstede's cultural dimensions theory, can help anticipate potential challenges. For example, companies from high power distance cultures may have different expectations regarding authority and hierarchy than those from low power distance cultures, which can affect how employees respond to new leadership or organizational changes.

Once the cultural assessment is complete, companies must identify the key cultural differences that could impact operations, decision-making, and employee engagement. This analysis should go beyond surface-level observations to identify deeper, more ingrained cultural differences that could create friction during the integration process. For example, differences in risk tolerance, collaboration styles, and work-life balance expectations can affect how employees from each organization approach their work. Understanding these differences is crucial for designing a cultural integration plan that addresses potential areas of conflict while promoting areas of alignment.

A detailed cultural integration plan should be developed early in the PMI process, outlining how the two cultures will be aligned and integrated. This plan should address both short-term integration goals—such as communication strategies and leadership alignment—and longer-term objectives—such as building a cohesive organizational culture that supports the merged company’s strategic goals.

Key components of a cultural integration plan include:

Leadership Alignment: Ensuring that leaders from both organizations are aligned in terms of vision, strategy, and communication. Leaders must model the desired behaviors and set the tone for cultural integration.

Communication Strategies: Clear and transparent communication is critical for reducing uncertainty and building trust during the integration process. Employees from both companies need to understand the rationale for the merger, the cultural changes that will occur, and how these changes will affect their roles. Regular updates, town halls, and feedback mechanisms are important for keeping employees informed and engaged.

Employee Engagement Programs: Employee engagement is crucial for fostering a cohesive culture in the post-merger organization. Programs that promote cross-company collaboration, team-building, and employee recognition can help bridge cultural differences and build a sense of unity. Additionally, retention strategies are important for ensuring that key talent stays with the company during the integration process.

Cultural integration is not a one-time event but an ongoing process that requires continuous monitoring and adaptation. Regular assessments of employee engagement, satisfaction, and collaboration should be conducted to gauge how well the cultural integration is progressing. Surveys and focus groups can help identify areas where additional support or intervention may be needed. Additionally, key performance indicators (KPIs) related to employee retention, productivity, and organizational alignment should be tracked to measure the success of the integration efforts.

Effective leadership plays a crucial role in managing cultural integration. Leaders must be culturally aware, adaptable, and committed to creating a shared vision for the merged organization. They must actively communicate the strategic objectives of the merger, model the desired cultural behaviors, and build consensus among employees from both companies. In many cases, leadership development programs or cross-cultural training may be necessary to equip leaders with the skills needed to navigate cultural differences effectively.

In cross-border mergers, where national cultural differences are particularly pronounced, leadership teams should be composed of representatives from both companies to ensure a balanced approach to decision-making and cultural alignment. This can help prevent one company’s culture from dominating the other and promote a more integrated and collaborative leadership style.

Cultural integration is a critical success factor in M&A, particularly in cross-border transactions where organizational and national cultural differences intersect. As demonstrated by the Daimler-Chrysler merger, failure to address cultural integration can have disastrous consequences, undermining the strategic objectives of the deal and leading to significant financial losses.

A strategic, robust, and comprehensive approach to cultural integration involves conducting thorough cultural assessments during the due diligence phase, identifying key areas of cultural difference, and developing a detailed integration plan that includes leadership alignment, clear communication, and employee engagement. Continuous monitoring and adaptation are essential to ensure that the cultural integration progresses smoothly and that the merged organization builds a cohesive, unified culture.

By combining academic insights from organizational culture theory and industry best practices, companies can manage cultural integration more effectively, reducing the risks of post-merger friction and increasing the likelihood of a successful and value-creating M&A transaction.

7.5. Overvaluation and Poor Financial Planning

Overvaluation and poor financial planning are two of the most critical and frequent financial missteps in mergers and acquisitions (M&A). These errors often stem from overly optimistic expectations, resulting in the acquirer paying a premium for a target company that is not supported by its future cash flows or synergies. This leads to financial underperformance and, in many cases, substantial financial write-offs or losses. A strategic, robust, and comprehensive understanding of these issues, incorporating academic insights from behavioral finance and industry best practices in financial modeling, can significantly reduce the risks associated with M&A transactions.

From an academic standpoint, overvaluation in M&A transactions is often linked to behavioral finance concepts, particularly overconfidence bias and hubris. Overconfidence bias refers to the tendency of executives to overestimate their ability to generate synergies or drive future growth from the acquisition. Research in behavioral finance suggests that this bias leads to an overestimation of the target’s value, pushing acquirers to pay premiums that cannot be justified by future earnings. This is particularly dangerous in competitive bidding situations, where herd behavior—another behavioral finance concept—can exacerbate overvaluation as multiple bidders drive up the price.

Hubris hypothesis, popularized by economist Richard Roll, further explains why acquirers might overpay for target companies. According to this theory, executives believe their superior management skills will enable them to generate value from the acquisition that others might miss. This leads to inflated valuations based on unrealistic assumptions of future success. However, the synergies that acquirers expect—whether through cost-cutting, revenue expansion, or operational efficiencies—are often overestimated or fail to materialize, resulting in financial losses.

A classic example of overvaluation driven by overconfidence bias is the 2011 acquisition of Autonomy by Hewlett-Packard (HP). HP paid $11.1 billion for Autonomy, a British software company, based on expectations of strong future revenue growth. However, less than a year later, HP wrote down $8.8 billion of the acquisition’s value due to accounting irregularities and overestimated revenue projections. This massive write-off illustrates the dangers of relying on overly optimistic financial assumptions and the failure to conduct adequate due diligence to verify the accuracy of the target’s financial statements. HP’s missteps highlight the need for realistic valuation assumptions and rigorous financial planning in M&A transactions.

Figure 7.7: Complexity of financial modeling technique in M&A.

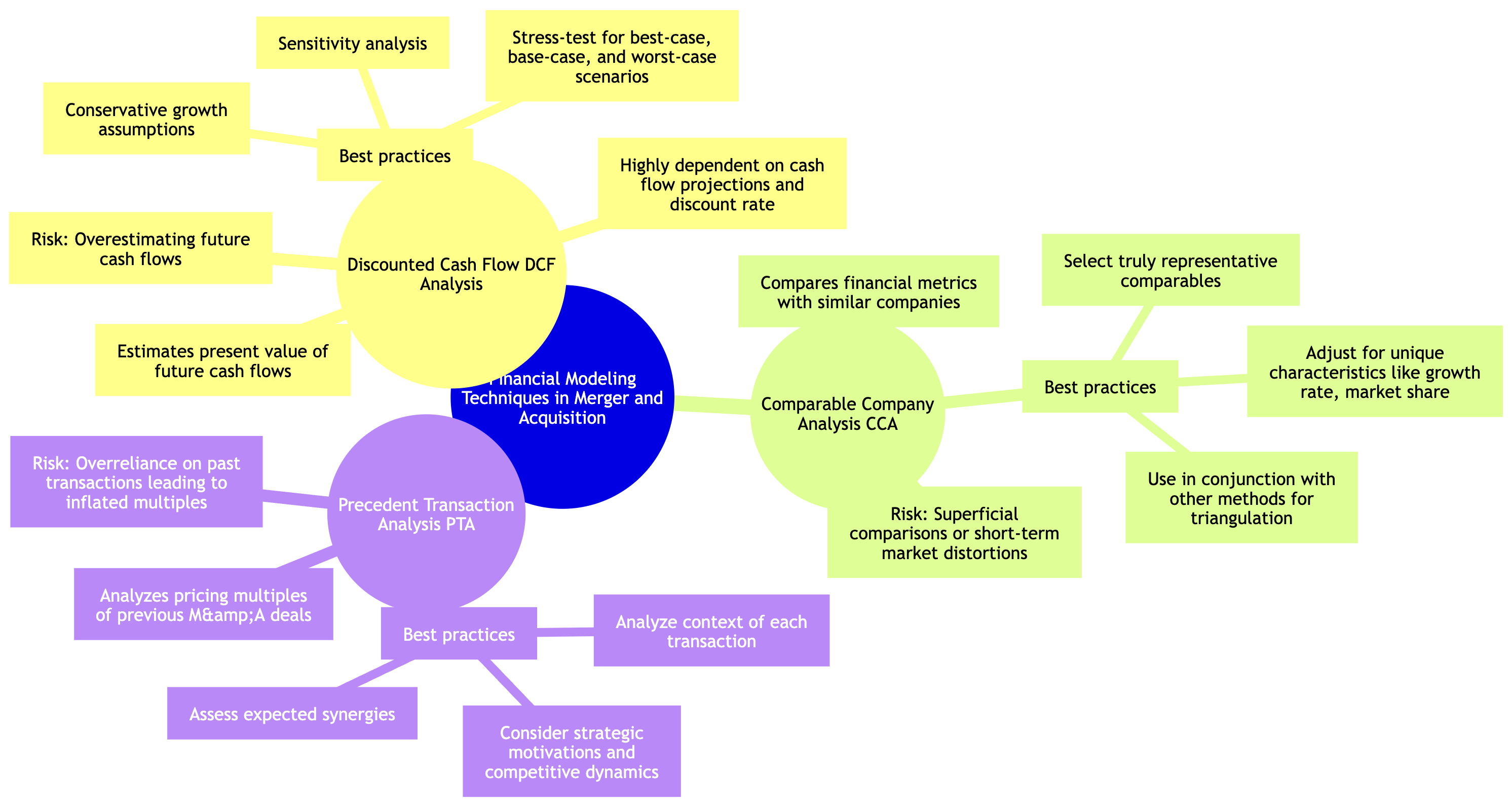

From an industry perspective, advanced financial modeling techniques—such as discounted cash flow (DCF) analysis, comparable company analysis (CCA), and precedent transaction analysis—are commonly used to estimate the value of a target company. However, while these models provide a structured framework for valuation, their accuracy depends on the quality of the assumptions they are built upon. Unrealistic assumptions about future revenue growth, cost synergies, and market conditions can lead to significant overvaluation, even when sophisticated models are employed.

Discounted cash flow (DCF) analysis is one of the most widely used methods for valuing companies in M&A. The DCF model estimates the present value of a target company’s future free cash flows, discounted back at an appropriate rate to account for the time value of money and risk. While theoretically sound, the reliability of a DCF analysis is highly dependent on the accuracy of the cash flow projections and the discount rate used. In many failed M&A deals, acquirers overestimate future cash flows by assuming unrealistic growth rates or underestimating the risks involved, leading to an inflated valuation. Industry best practice for conducting a DCF analysis involves adopting conservative growth assumptions and testing multiple discount rates to account for market volatility and uncertainty. Additionally, acquirers should conduct sensitivity analysis—a process that tests how changes in key variables, such as revenue growth, operating margins, and discount rates, impact the valuation. By stress-testing these assumptions under best-case, base-case, and worst-case scenarios, acquirers can develop a more robust understanding of the range of possible outcomes and reduce the risk of overvaluation.

Comparable company analysis (CCA) is another common valuation method that involves comparing the target company’s financial metrics—such as earnings before interest, taxes, depreciation, and amortization (EBITDA) or price-to-earnings (P/E) ratios—with those of similar companies in the same industry. While this method provides a market-based valuation benchmark, it is crucial to ensure that the comparables selected are truly representative of the target company’s size, growth prospects, and risk profile. Industry best practice in applying CCA involves adjusting the valuation multiples for any unique characteristics of the target company, such as its growth rate, market share, or exposure to industry-specific risks. This helps to avoid superficial comparisons that might overstate or understate the target’s value. Additionally, CCA should be used in conjunction with other valuation methods to triangulate a fair purchase price, rather than relying solely on market comparables, which can sometimes reflect short-term market distortions or irrational investor behavior.

Precedent transaction analysis examines the pricing multiples of previous M&A deals involving similar companies. This approach can be useful for understanding how much other acquirers have been willing to pay for similar targets in the past. However, just as with CCA, relying too heavily on precedent transaction data can lead to overvaluation if the market conditions or strategic rationale for past deals are no longer relevant. Best practice in precedent transaction analysis involves carefully analyzing the context of each transaction, including the strategic motivations of the buyer, the competitive dynamics at the time, and the synergies that were expected to result from the acquisition. Without understanding the specific circumstances behind past transactions, there is a risk of applying inflated multiples to the current deal, leading to an unjustified premium.

Beyond valuation, financial planning in M&A must account for the costs of integration, the risks of achieving synergies, and potential market volatility. Even if the target company is fairly valued, poor financial planning can lead to unexpected costs or delayed benefits, eroding the financial rationale for the deal.

One of the most common pitfalls in M&A financial planning is the overestimation of synergies—the cost savings or revenue enhancements expected to result from the merger. Many acquirers assume that integrating the two companies will result in immediate cost reductions or new revenue streams, but these synergies often prove elusive. For example, cost synergies from consolidating IT systems, streamlining supply chains, or eliminating redundant staff may take longer to realize or may be more expensive than anticipated. Similarly, revenue synergies—such as cross-selling opportunities or expanding into new markets—may not materialize if customer bases or distribution channels are more difficult to integrate than expected. Best practice for synergy estimation involves building conservative assumptions into the financial model, acknowledging the integration challenges that may arise. Acquirers should also develop a detailed integration plan that includes clear milestones and timelines for achieving synergies, as well as contingency plans for managing delays or setbacks. Realistic synergy estimates, grounded in data from past integrations, help to ensure that the financial projections are achievable and that the deal delivers the expected value.

Another critical aspect of financial planning in M&A is preparing for market volatility and other external risks. Even if the target company’s value is fairly assessed, unexpected changes in market conditions—such as an economic downturn, shifts in regulatory policy, or new competitive threats—can dramatically affect the outcome of the deal. Sensitivity analysis and scenario planning are essential tools for managing these risks. By modeling multiple financial scenarios, including best case, base case, and worst case, acquirers can better understand how different market conditions might impact the financial performance of the target company. This allows decision-makers to adjust their strategy if conditions change and to ensure that the company is not over-reliant on overly optimistic assumptions.

Overvaluation and poor financial planning are frequent and costly errors in M&A transactions, but they can be mitigated through a strategic, robust, and comprehensive approach to financial management. By incorporating behavioral finance insights to counteract biases like overconfidence, and by applying industry best practices in financial modeling, companies can avoid paying excessive premiums for target companies and develop more realistic expectations for synergies and integration costs.

A successful M&A transaction requires realistic valuation assumptions, conservative synergy estimates, and detailed financial planning that includes sensitivity analysis and scenario planning to account for market volatility. By grounding their approach in both academic theory and practical industry experience, companies can significantly reduce the financial risks associated with M&A and improve their chances of delivering long-term value from the transaction.

7.6. Case Studies – High-Profile Failures in the Digital Industry

The digital industry, with its rapid pace of innovation and technological disruption, has witnessed some of the most high-profile mergers and acquisitions (M&A) failures in recent years. Deals that initially promised to create industry powerhouses have often fallen apart due to misaligned strategies, cultural incompatibilities, and poor financial planning. Two prominent examples—the AOL-Time Warner merger in 2000 and HP’s acquisition of Autonomy in 2011—illustrate the challenges companies face when navigating M&A in the digital sector. These failures offer critical lessons on how to improve M&A strategy, particularly in fast-moving, tech-driven industries.

The AOL-Time Warner merger, valued at $350 billion, was initially hailed as a groundbreaking deal. The idea was to combine “old media”—Time Warner’s vast library of content, film studios, and cable network—with the “new media” promise of AOL’s dominant internet service and user base. The merger was intended to create a vertically integrated media and technology giant capable of dominating the digital content landscape. However, the deal quickly unraveled and is now regarded as one of the biggest failures in M&A history. The reasons for this failure offer valuable strategic lessons for future transactions in the digital space.

From an academic perspective, the AOL-Time Warner merger suffered from strategic misalignment. Resource-based view (RBV) theory suggests that successful acquisitions require a clear alignment of resources and capabilities that complement each other to create a competitive advantage. In the case of AOL-Time Warner, the synergies anticipated between the two companies were based on overly optimistic assumptions about the convergence of media and technology. AOL’s internet service and Time Warner’s content libraries were not as easily integrated as originally envisioned, and the synergies that were supposed to result from the merger—such as the cross-promotion of content and the monetization of digital assets—failed to materialize.

Moreover, behavioral finance theory—specifically overconfidence bias—can help explain the overestimation of these synergies. Executives at both companies believed that the combined entity would dominate the new digital landscape, but they failed to account for technological disruptions and market volatility, especially the bursting of the dot-com bubble in 2000. This external shock eroded AOL’s stock value, undermined investor confidence, and drastically reduced the financial viability of the merger.

In practice, the failure of AOL-Time Warner demonstrates the need for realistic financial planning and scenario analysis in M&A deals. Companies must be cautious about making overly optimistic projections about synergies, particularly in industries characterized by rapid technological change. Sensitivity analysis and scenario planning could have helped the companies model different outcomes—such as market downturns or slower-than-expected convergence of old and new media—and provided a more realistic basis for decision-making.

Cultural clash was another major factor in the failure of the AOL-Time Warner merger. AOL, as a fast-moving, internet-driven company, had a decentralized, informal, and entrepreneurial culture, while Time Warner operated as a traditional media conglomerate with a more hierarchical and structured corporate environment. This cultural mismatch created friction across management levels, leading to divergent approaches to decision-making, innovation, and leadership. Research in organizational behavior suggests that cultural integration is a key determinant of M&A success, and the AOL-Time Warner case illustrates how differences in corporate culture can derail even the most strategically sound deals.

In terms of industry best practices, conducting a cultural audit during the due diligence phase is essential for identifying potential areas of conflict. Cultural audits involve assessing the core values, norms, and leadership styles of both organizations to determine how well they align. In the case of AOL-Time Warner, more attention to these cultural differences might have led to a more proactive integration strategy, where efforts were made to bridge cultural divides through leadership training, communication programs, and organizational change management.

HP’s 2011 acquisition of Autonomy, valued at $11.1 billion, was another high-profile failure in the digital industry, underscoring the dangers of overvaluation and inadequate due diligence. HP’s acquisition strategy was aimed at bolstering its software offerings, moving beyond its hardware-focused business to tap into Autonomy’s enterprise software and data analytics capabilities. However, less than a year after the deal closed, HP wrote down $8.8 billion of the acquisition’s value due to accounting irregularities, overestimated revenue projections, and failed integration efforts. The fallout from the Autonomy acquisition highlights several key issues that companies must address in the M&A process.

The overvaluation of Autonomy was a critical factor in the deal’s failure. HP’s leadership believed that Autonomy would drive future revenue growth in the rapidly expanding enterprise software market. However, HP failed to conduct sufficient due diligence to verify the accuracy of Autonomy’s financial statements, which were later found to include accounting irregularities that inflated revenue and profitability figures.

From an academic standpoint, the winner’s curse—a concept in auction theory—helps explain why HP overpaid for Autonomy. In competitive bidding scenarios, the “winner” often pays more than the intrinsic value of the target because they base their bid on overly optimistic assumptions or incomplete information. In HP’s case, behavioral finance biases such as overconfidence likely contributed to the decision to proceed with the acquisition despite red flags in Autonomy’s financial reports.

Industry best practices for mitigating overvaluation risks include conducting thorough forensic accounting reviews and engaging independent auditors to verify the financial health of the target. Advanced financial modeling techniques, such as discounted cash flow (DCF) analysis and sensitivity analysis, should be used to test multiple financial scenarios and assess how different revenue growth rates and cost assumptions affect the valuation. HP’s failure to perform these rigorous due diligence steps contributed to the deal’s collapse.

Beyond financial missteps, the integration challenges between HP and Autonomy were another major factor in the failure of the deal. HP underestimated the complexities of integrating Autonomy’s software solutions into its existing portfolio, leading to operational inefficiencies and delayed synergies. Autonomy’s leadership, which had been integral to the company’s success, clashed with HP’s management, leading to the departure of key personnel and a loss of institutional knowledge.

Post-merger integration (PMI) is critical to realizing the value of any acquisition, especially in technology-driven industries where technological compatibility and talent retention are essential to success. HP’s failure to integrate Autonomy effectively illustrates the need for a comprehensive integration plan that addresses not only technological systems but also leadership, culture, and operational processes. In industry practice, successful integration often involves establishing a dedicated integration team or Integration Management Office (IMO) to oversee the process and ensure that synergies are realized according to a clear timeline and set of milestones.

For companies operating in the fast-moving digital industry, these case studies provide critical lessons about the importance of strategic fit, technological compatibility, and cultural alignment in M&A transactions. Unlike traditional industries, where mergers may focus primarily on scale or market expansion, digital companies must also navigate rapid technological advancements and market disruptions that can quickly undermine the value of a deal.

In the digital sector, assessing the strategic fit between the acquirer and the target goes beyond traditional financial metrics. It requires a deep understanding of the target’s technological capabilities and how they align with the acquirer’s long-term strategy. M&A deals in this space should prioritize technological compatibility to ensure that the target’s software, systems, and data can be seamlessly integrated with the acquirer’s existing infrastructure. For example, if the target operates on a completely different technology stack, the integration costs and challenges may outweigh the potential synergies, as was the case in HP’s acquisition of Autonomy.

In practice, conducting a technology audit during due diligence is essential for identifying potential integration challenges. This audit should assess the compatibility of IT systems, data architectures, and software platforms to ensure that the integration can be executed smoothly. Companies must also account for technological disruption—such as the emergence of new technologies or changes in industry standards—that could affect the future viability of the target’s solutions.

The AOL-Time Warner merger underscores the importance of cultural alignment in digital M&A deals, particularly when combining organizations with different corporate histories, leadership styles, and approaches to innovation. In fast-moving industries like technology, cultural alignment is crucial for fostering innovation and collaboration in the post-merger organization. A lack of alignment can stifle creativity, reduce employee engagement, and slow down decision-making, leading to missed opportunities and delayed synergies.

To ensure cultural alignment, companies must conduct cultural audits during due diligence and develop a cultural integration plan that aligns leadership, communication practices, and employee engagement programs. Change management strategies that involve employees from both organizations in the integration process can help bridge cultural divides and foster a unified post-merger culture.

Finally, realistic synergy expectations are essential to avoiding the financial pitfalls that have plagued digital M&A deals. Overestimating synergies—whether in the form of cost savings, revenue growth, or market expansion—can lead to overvaluation and post-merger disappointment. Companies must adopt conservative assumptions about synergies and use sensitivity analysis to model different scenarios, ensuring that the deal delivers value even in less favorable market conditions.

By adopting these strategic, robust, and comprehensive practices, companies in the digital industry can improve their chances of executing successful M&A transactions that create long-term value, even in the face of rapid technological change and market disruption.

7.7. Case Studies – Missteps in Oil & Gas Mergers

The oil and gas industry presents a distinct set of challenges for mergers and acquisitions (M&A) due to its inherent market volatility, stringent regulatory environment, and the sheer scale of operational integration required. Deals in this sector often involve large, capital-intensive assets, complex global supply chains, and significant stakeholder scrutiny, making integration particularly complex. The 1998 merger between BP and Amoco and the 2016 merger between Royal Dutch Shell and BG Group offer valuable lessons for navigating these challenges. Both examples underscore the need for strategic planning, robust integration frameworks, and adaptive strategies to manage the specific risks of this industry.

One of the most significant challenges in oil and gas M&A is dealing with market volatility, particularly fluctuations in oil prices. Since oil prices are influenced by a wide range of factors—including geopolitical tensions, global supply and demand, and regulatory changes—M&A deals in this sector are especially vulnerable to shifts in market conditions. Fluctuating oil prices can alter the financial assumptions underpinning a deal, leading to unexpected revenue shortfalls, cost overruns, and delayed synergies.

In the case of the Royal Dutch Shell and BG Group merger, the $70 billion deal was completed during a period of relatively high oil prices. However, shortly after the merger, oil prices dropped significantly, putting pressure on Shell’s ability to achieve the expected returns from the acquisition. This highlighted the need for scenario planning and financial modeling that accounts for market volatility.

From an academic perspective, real options theory is particularly relevant in the oil and gas sector. This theory views investment decisions, such as M&A, as a series of options that unfold over time, allowing companies to adapt to changing market conditions. In practice, this means acquirers should build flexibility into their financial models and stress-test assumptions against multiple market scenarios. For instance, by modeling oil prices at different levels (e.g., $40, $60, and $80 per barrel), companies can better understand the financial risks and opportunities under various market conditions. Sensitivity analysis—which tests how changes in key variables (like oil prices or production costs) affect the deal’s value—helps ensure that M&A decisions are robust even in the face of market uncertainty.

The oil and gas industry is subject to intense regulatory scrutiny, ranging from environmental regulations to foreign ownership restrictions. The complexity of these regulatory environments often increases when deals involve cross-border transactions, adding additional layers of compliance. Failing to navigate these regulatory hurdles can lead to delays in deal closure, operational restrictions, or even deal cancellations.

For instance, in the BP-Amoco merger, the companies had to navigate complex regulatory environments across multiple jurisdictions, given their vast global operations. Ensuring compliance with environmental laws, antitrust regulations, and labor standards across different countries required substantial legal and operational planning.

Industry best practices for managing regulatory risks include conducting regulatory due diligence as part of the broader M&A due diligence process. This involves assessing the regulatory frameworks in each jurisdiction where the target company operates, identifying potential compliance risks, and determining whether additional regulatory approvals are required for the deal to proceed. Additionally, post-merger, companies must develop strategies for harmonizing regulatory compliance across the combined entity, particularly when the two companies operate under different legal regimes.

Academic research into transaction cost economics highlights the importance of understanding regulatory costs as part of the M&A process. Companies in highly regulated industries like oil and gas face higher transaction costs due to the need for regulatory approvals, ongoing compliance efforts, and the risk of regulatory penalties. Building a clear regulatory strategy into the M&A process can help mitigate these costs and ensure that the deal delivers value.

Cultural misalignment is a recurring theme in M&A failures across industries, but it poses particular challenges in the oil and gas sector, where companies often have long-established cultures shaped by their specific operational environments. For example, companies that focus heavily on upstream activities (exploration and production) may have a very different culture from those focused on downstream operations (refining and distribution), which can create tensions during integration.

In the BP-Amoco merger, cultural differences between the two companies—BP’s British roots and hierarchical structure, and Amoco’s more decentralized, American-style management—became a significant source of friction during integration. This misalignment affected decision-making processes, leadership styles, and employee engagement, ultimately contributing to operational inefficiencies and underperformance.

Academic literature on organizational behavior and cultural integration emphasizes that M&A success requires a deliberate effort to align the cultures of the two companies. Research suggests that companies should conduct cultural due diligence alongside financial and operational due diligence. This involves assessing the values, leadership styles, and working norms of both organizations to identify potential areas of conflict. Cultural misalignments, if left unchecked, can lead to employee turnover, miscommunication, and delays in achieving synergies.

From an industry practice standpoint, successful cultural integration involves developing a cultural integration plan early in the M&A process. This plan should address key issues such as leadership alignment, decision-making frameworks, and employee engagement strategies. For large-scale mergers like those in the oil and gas industry, cultural alignment is particularly important in global operations, where differences in national cultures and corporate practices can further complicate integration efforts. Tools like cultural surveys, leadership training, and team-building initiatives can help bridge these gaps and create a more cohesive post-merger organization.

Operational integration in the oil and gas industry is particularly challenging due to the capital-intensive nature of the sector and the complexity of global supply chains. Integrating the operations of two large-scale organizations requires careful coordination of production facilities, logistics networks, and technology systems. Failure to manage these operational complexities can lead to significant cost overruns, delays, and inefficiencies.

The Royal Dutch Shell and BG Group merger provides a useful example of the operational challenges inherent in oil and gas M&A. While the deal was strategically sound—allowing Shell to expand its liquefied natural gas (LNG) portfolio—the integration of the two companies' operations proved more complex than anticipated. Issues such as cost management and alignment of operational structures delayed the realization of synergies, and the fluctuating oil prices during this period further complicated the integration process.

In practice, effective operational integration in the oil and gas sector requires a phased approach that prioritizes critical areas such as production efficiency, supply chain optimization, and technology integration. Companies should establish a dedicated integration management office (IMO) to oversee the process and ensure that integration milestones are met. Additionally, industry best practices suggest the use of integration playbooks, which outline the specific steps required to harmonize operational processes, technologies, and supply chains across the two companies.

From an academic perspective, lean operations theory and supply chain integration frameworks offer insights into how companies can streamline their operations post-merger. Lean operations focuses on reducing waste and improving efficiency, which is particularly important in capital-intensive industries like oil and gas. Supply chain integration theory emphasizes the need for collaboration across supply chain partners, particularly in global industries where disruptions in one part of the chain can have ripple effects across the entire operation.

Finally, adapting to market conditions is critical for ensuring the long-term success of M&A in the oil and gas industry. Given the cyclical nature of oil prices and the increasing push for renewable energy, companies must be flexible in how they manage post-merger integration and strategy. The Shell-BG merger occurred just as the oil market was undergoing significant changes, with lower oil prices affecting the profitability of traditional oil and gas operations and raising questions about the future viability of fossil fuel-based business models.

Scenario planning is an essential tool for adapting to these market conditions. By modeling different market scenarios—including oil price fluctuations, shifts in regulatory environments, and changes in energy demand—companies can develop strategies that are flexible and resilient. For example, companies might explore diversification into renewable energy or adjust capital expenditure based on oil price forecasts.

From an industry perspective, companies that engage in long-term strategic planning—including energy transition scenarios—are better positioned to navigate market volatility. This is particularly important as the global energy landscape continues to shift towards sustainability and decarbonization. The ability to pivot and adapt to these market dynamics is essential for ensuring that M&A transactions remain viable and deliver long-term value.

The oil and gas industry’s unique set of challenges—including market volatility, regulatory hurdles, cultural alignment, and large-scale operational integration—make M&A transactions particularly complex. The failures and challenges observed in the BP-Amoco and Royal Dutch Shell-BG mergers offer valuable lessons for improving M&A strategy in this sector.

Figure 7.8: Lesson learn from M&A failure in oil and gas industry.

Rigorous financial planning that accounts for market volatility through scenario planning and sensitivity analysis.

Navigating regulatory risks with a thorough understanding of compliance requirements across multiple jurisdictions.

Cultural due diligence and integration plans that address leadership alignment and employee engagement.

Operational integration frameworks that prioritize efficiency and technology alignment.

Adaptability to changing market conditions, particularly as the global energy sector evolves toward renewable energy sources.

By combining academic insights with industry best practices, companies in the oil and gas sector can improve their chances of executing successful M&A deals that create long-term value, even in the face of significant operational and market challenges.

7.8. Conclusion

The lessons learned from M&A failures are critical for companies seeking to improve their M&A strategies and avoid the common pitfalls that lead to underperformance or outright failure. Common causes of M&A failure—such as overvaluation, poor financial planning, cultural clashes, and lack of strategic fit—can be mitigated through rigorous due diligence, realistic financial modeling, and effective post-merger integration. By analyzing high-profile failures in industries such as digital and oil & gas, companies can develop a deeper understanding of the specific challenges these sectors face in M&A transactions. Ultimately, learning from past failures allows companies to build more sustainable and successful M&A strategies that support long-term growth and value creation.

7.8.1. Further Learning with GenAI

These prompts encourage deep exploration of both theoretical frameworks and practical strategies to understand M&A failures and avoid common pitfalls. They aim to provoke advanced, multifaceted answers that incorporate financial modeling, cultural integration, operational alignment, risk management, and strategic communication—all critical factors for successful M&A outcomes.

How can companies build a robust framework for preventing M&A failure by integrating lessons from behavioral finance theories like the winner’s curse, overconfidence bias, and herding behavior into their decision-making and valuation processes?

What specific strategies can companies employ to avoid overvaluation in M&A deals, considering factors like fluctuating market conditions, future growth projections, and synergy overestimation? How do advanced financial models and sensitivity analysis improve accuracy?

In the context of cross-border M&A, how can companies assess and manage the complex challenges of cultural integration, and what specific metrics or diagnostic tools can be used to predict cultural compatibility and reduce post-merger integration risks?

How can companies apply scenario analysis and real options theory to anticipate and mitigate potential M&A deal failures in volatile industries, and what advanced risk management strategies can be used to hedge against unforeseen operational or market risks?

What role does due diligence in intangible assets—such as intellectual property, brand value, and customer loyalty—play in preventing M&A failure, and how can companies more accurately measure and incorporate these into their valuation and integration planning processes?

What lessons can be drawn from high-profile digital industry M&A failures, like AOL-Time Warner and HP-Autonomy, in terms of misaligned strategic goals, technology integration challenges, and leadership failures? How can these insights guide future tech sector M&A strategies?

How can companies in capital-intensive industries like oil and gas leverage advanced operational risk management frameworks, including predictive analytics and machine learning, to anticipate integration issues and avoid the common pitfalls seen in past industry M&A failures?

What are the best methods for conducting a comprehensive cultural audit pre-merger, and how can companies systematically address leadership, communication, and decision-making style differences to minimize cultural clashes during post-merger integration?

How do academic theories on organizational change management, such as Lewin's Change Model and Kotter’s 8-Step Process, apply to M&A integration planning, and how can these frameworks be adapted to facilitate smoother cultural and operational alignment post-merger?

What advanced valuation techniques (e.g., real options analysis, Monte Carlo simulations) can companies employ to avoid overestimating synergies or future growth in M&A transactions, particularly in fast-moving industries like technology or pharmaceuticals?

How can companies integrate environmental, social, and governance (ESG) considerations into their M&A strategy to avoid long-term reputational and regulatory risks, particularly in industries where ESG issues are increasingly critical, such as energy or consumer goods?

What are the key financial and operational metrics that companies should track during the post-merger integration phase to ensure that the projected synergies are being realized, and how can advanced monitoring tools like dashboards and KPIs help to avoid underperformance?

How can companies avoid the trap of misaligned incentives in M&A, where executives pursue deals that maximize short-term personal gains rather than long-term shareholder value, and how can governance structures and performance-based compensation be aligned to ensure accountability?