Chapter 5

Comprehensive Due Diligence Scopes

"Due diligence is the cornerstone of successful M&A. It’s not just about mitigating risks—it’s about uncovering hidden opportunities that can drive long-term value and sustainable growth. In today’s market, companies that integrate financial, operational, and ESG factors into their due diligence process are the ones that consistently outperform." — Jane Doe, Managing Director, Global M&A Advisory, Deloitte

This chapter provides a comprehensive guide to conducting due diligence in mergers and acquisitions, covering all critical areas such as business, financial, legal, tax, operational, and ESG factors. By ensuring a thorough understanding of the target company’s strengths, risks, and opportunities, the acquiring company can mitigate potential risks while identifying areas for value creation. The chapter emphasizes the importance of aligning the due diligence process with the acquirer’s long-term strategic goals, ensuring that the acquisition supports both immediate and future growth.

5.1. The Critical Role of Scientific Due Diligence in M&A

Due diligence serves as the cornerstone of informed decision-making in mergers and acquisitions (M&A), providing a systematic, rigorous, and scientific basis for evaluating potential deals. It is through this meticulous process that acquiring companies gain a comprehensive understanding of the target's true value, potential risks, and alignment with long-term strategic objectives. The complexity of M&A transactions necessitates that due diligence extends far beyond basic financial assessments, encompassing an exhaustive evaluation of the target company's business operations, market positioning, financial health, legal standing, operational infrastructure, technological capabilities, and environmental, social, and governance (ESG) practices. A well-executed due diligence process ensures that the acquisition not only delivers immediate financial returns but also contributes to sustainable, long-term value creation.

Figure 5.1: Common academic theories for Due Diligence.

From an academic standpoint, several strategic management theories offer valuable insights into the due diligence process, guiding the assessment of a target company's value and potential fit with the acquirer’s strategic goals. Among the most influential are the resource-based view (RBV), dynamic capabilities theory, agency theory, and corporate governance principles.

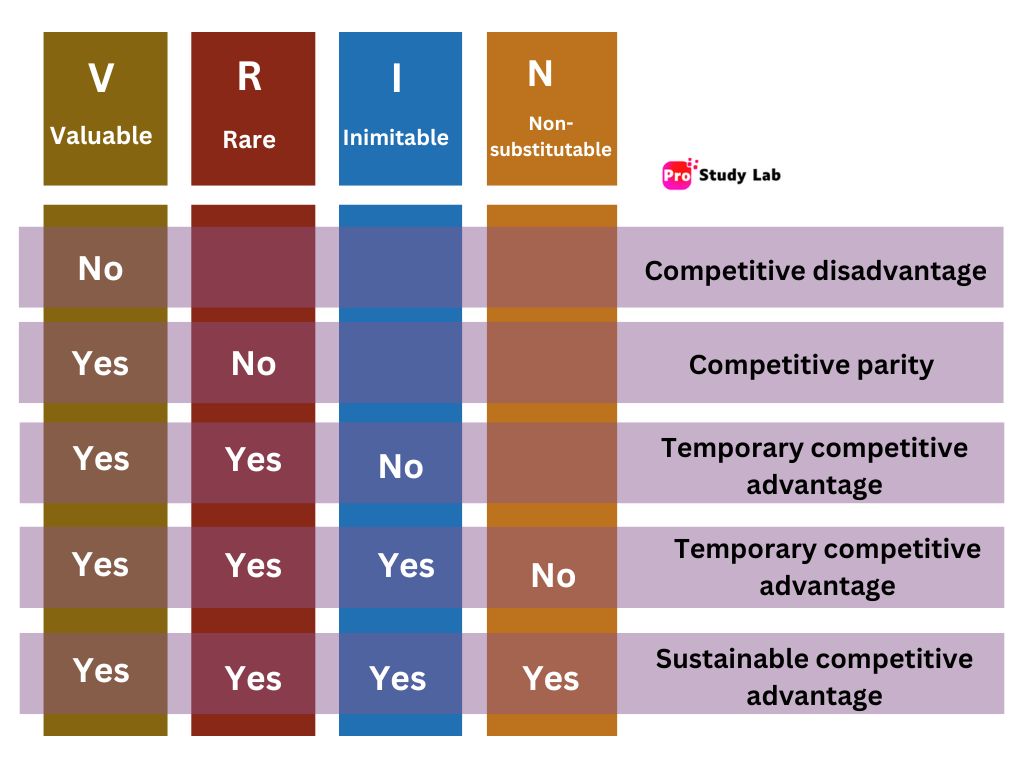

Resource-Based View (RBV): The resource-based view (RBV) posits that a firm’s sustained competitive advantage stems from its ability to acquire and leverage resources that are valuable, rare, inimitable, and non-substitutable (VRIN). In the context of M&A due diligence, RBV emphasizes the importance of identifying whether the target company possesses resources—such as proprietary technologies, brand equity, human capital, or unique operational capabilities—that can enhance the acquiring company's strategic position. By focusing on these VRIN resources during the due diligence process, the acquiring company can ensure that the target’s assets will provide a meaningful and sustainable competitive advantage post-merger. For example, when Microsoft acquired LinkedIn, the due diligence process focused on LinkedIn’s vast professional network, data analytics capabilities, and strong brand presence, which aligned with Microsoft’s vision to enhance its cloud and enterprise offerings. The integration of LinkedIn’s resources provided Microsoft with a unique competitive edge in the professional services market, demonstrating the value of leveraging RBV in the due diligence process.

Figure 5.2: VRIN framework for RBV theory.

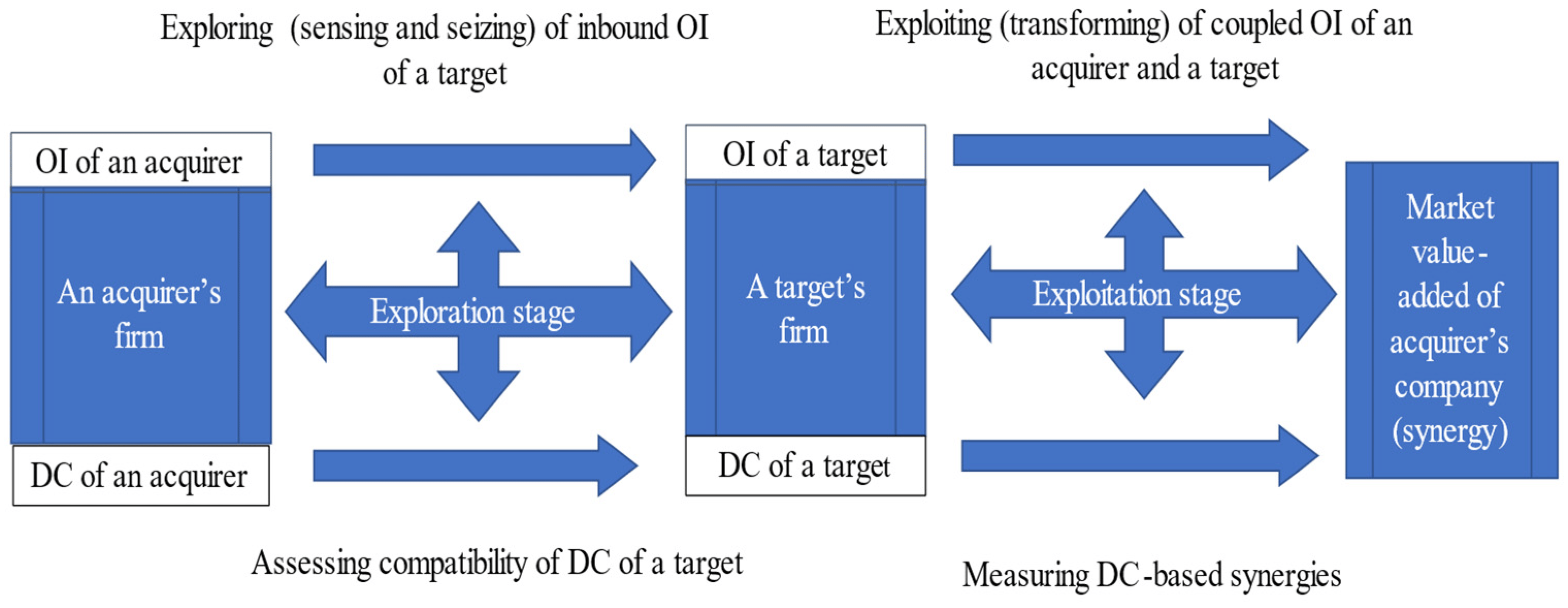

Dynamic Capabilities Theory: This introduced by David Teece, builds on RBV by emphasizing the need for firms to continuously adapt, integrate, and reconfigure their resources to respond to changing market conditions. In M&A due diligence, this theory underscores the importance of assessing the target company's ability to adapt to technological disruptions, evolving customer preferences, and market shifts. It is not enough to acquire resources; the acquiring company must determine whether it can effectively integrate and leverage those resources to maintain agility and competitiveness in a dynamic business environment. For instance, when Amazon acquired Whole Foods, the due diligence process involved evaluating not only Whole Foods’ existing supply chain and retail capabilities but also how these capabilities could be integrated into Amazon’s e-commerce platform to create a more adaptive and innovative grocery delivery model. The successful integration of Whole Foods’ assets into Amazon’s dynamic capabilities allowed Amazon to expand its footprint in the grocery sector, illustrating the importance of this theoretical approach in due diligence.

Figure 5.3: Dynamic capability (DC) assessment in M&A.

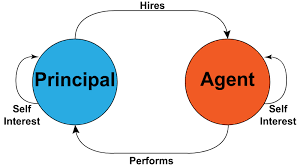

Agency Theory: This explores the relationship between principals (shareholders) and agents (management) and the conflicts that can arise when their interests are not aligned. In M&A, agency theory becomes relevant in assessing whether the target company's management has acted in the best interests of its shareholders, as well as in evaluating the governance structures that are in place. Due diligence should include an analysis of the target's executive compensation, decision-making processes, and any potential conflicts of interest that could affect the deal’s success. Agency theory suggests that acquiring companies must investigate whether the target's management has been incentivized to maximize shareholder value or whether they might have engaged in self-serving behaviors, such as excessive risk-taking or short-term profit maximization. Understanding these dynamics is crucial for ensuring that the post-merger integration process aligns with the acquiring company’s long-term objectives and minimizes potential conflicts.

Figure 5.4: Self-interest common problem in agency theory.

Corporate Governance Principles: These provide a framework for evaluating the target company's governance structure, risk management practices, and adherence to ethical standards. Effective due diligence should examine the target's board composition, ownership structure, audit practices, and compliance with regulatory requirements. By evaluating these elements, the acquiring company can assess the target's governance quality, transparency, and accountability, which are critical for mitigating risks and ensuring successful integration. For example, when Unilever acquired Seventh Generation, it conducted thorough due diligence on the target’s governance practices, ethical standards, and commitment to sustainability. This ensured that Seventh Generation’s values aligned with Unilever’s corporate governance principles, facilitating a smoother integration process and reinforcing Unilever's commitment to sustainable growth.

Figure 5.6: Main aspects of corporate governance.

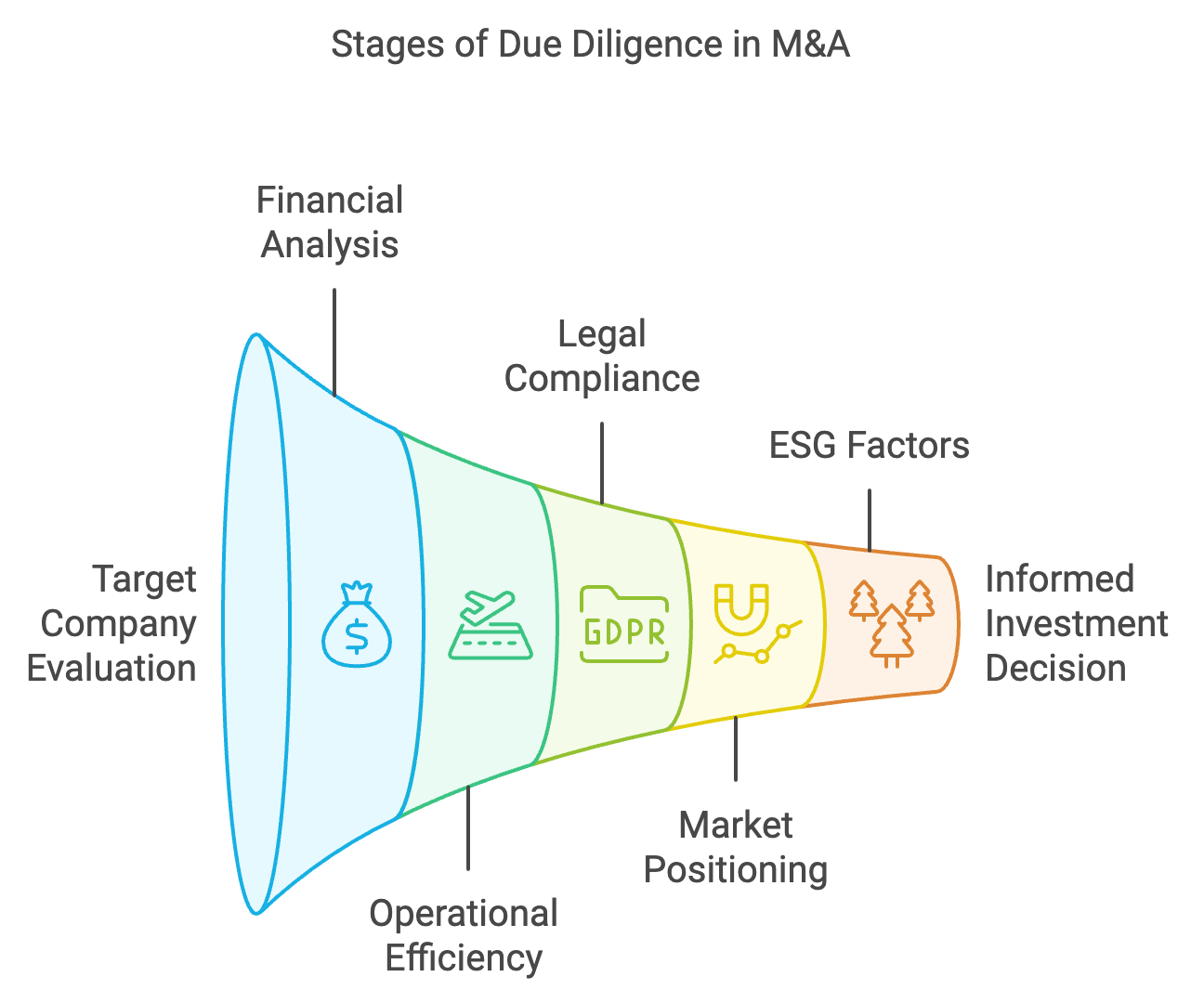

In practice, due diligence involves a structured, multifaceted process that combines both quantitative and qualitative analyses. The objective is to gain a holistic view of the target company's strengths, weaknesses, opportunities, and threats (SWOT) to make an informed investment decision. The following are some of the key dimensions of due diligence that industry practitioners focus on:

Figure 5.7: Main stages of due diligence process.

Financial due diligence is a fundamental aspect of M&A, involving an in-depth analysis of the target company's financial statements, revenue streams, profitability, cash flow, debt levels, and capital expenditure requirements. This process provides insights into the financial health and sustainability of the target’s business model. Practitioners employ methods such as discounted cash flow (DCF) analysis, comparable company analysis, and precedent transaction analysis to assess the target's valuation and ensure that the acquisition price reflects its true value. Financial due diligence also involves stress-testing the target’s financials under different market scenarios to identify potential risks, such as economic downturns or changes in interest rates. This helps the acquiring company anticipate potential challenges and avoid overpaying for the target.

Operational due diligence involves evaluating the target's operational efficiency, production capabilities, supply chain management, IT infrastructure, and human resources. This process is essential for identifying potential integration challenges, such as system incompatibilities, process inefficiencies, or workforce redundancies. It also enables the acquiring company to identify opportunities for cost savings, process optimization, and scalability post-acquisition. For example, when Disney acquired 21st Century Fox, operational due diligence played a crucial role in understanding how Fox’s content production, distribution networks, and digital platforms could be integrated with Disney's existing operations to achieve synergies and create value.

Legal due diligence focuses on identifying potential legal liabilities, regulatory compliance issues, intellectual property rights, and contractual obligations. This process ensures that the target is free from legal disputes, regulatory penalties, or contractual breaches that could jeopardize the deal’s success. Companies should engage legal experts to review the target’s contracts, patents, trademarks, litigation history, and compliance with labor, environmental, and antitrust regulations. In cross-border deals, legal due diligence must also address the complexities of navigating different legal frameworks, trade restrictions, and foreign investment regulations. This ensures that the acquiring company is aware of any potential legal obstacles and can develop strategies to address them.

Market due diligence involves evaluating the target’s market positioning, competitive landscape, customer base, and growth prospects. This process helps the acquiring company understand the target’s competitive strengths, market share, and potential for revenue growth. It also identifies potential market risks, such as changing customer preferences, emerging competitors, or technological disruptions. By conducting market due diligence, the acquiring company can assess whether the target's business model is sustainable and whether the acquisition will enhance its market positioning. This aspect of due diligence is particularly critical in fast-evolving industries, such as technology and healthcare, where market dynamics can change rapidly.

ESG due diligence has become a key component of M&A transactions recently, reflecting the growing emphasis on sustainability, corporate responsibility, and ethical practices. ESG due diligence involves evaluating the target's environmental impact, social practices, and governance standards to ensure alignment with the acquiring company’s values and sustainability goals. This includes assessing the target’s carbon footprint, labor practices, community engagement, and adherence to ethical standards. Companies that prioritize ESG due diligence are better positioned to avoid reputational risks, regulatory penalties, and operational challenges, while also enhancing their brand value and stakeholder trust.

The due diligence process must be grounded in scientific and systematic methods to ensure objectivity, thoroughness, and accuracy. By leveraging academic frameworks, quantitative models, and qualitative assessments, companies can make more informed decisions and minimize the risks associated with M&A. For instance, conducting scenario analysis, sensitivity analysis, and Monte Carlo simulations can provide a deeper understanding of the potential risks and opportunities associated with the target company’s financial performance.

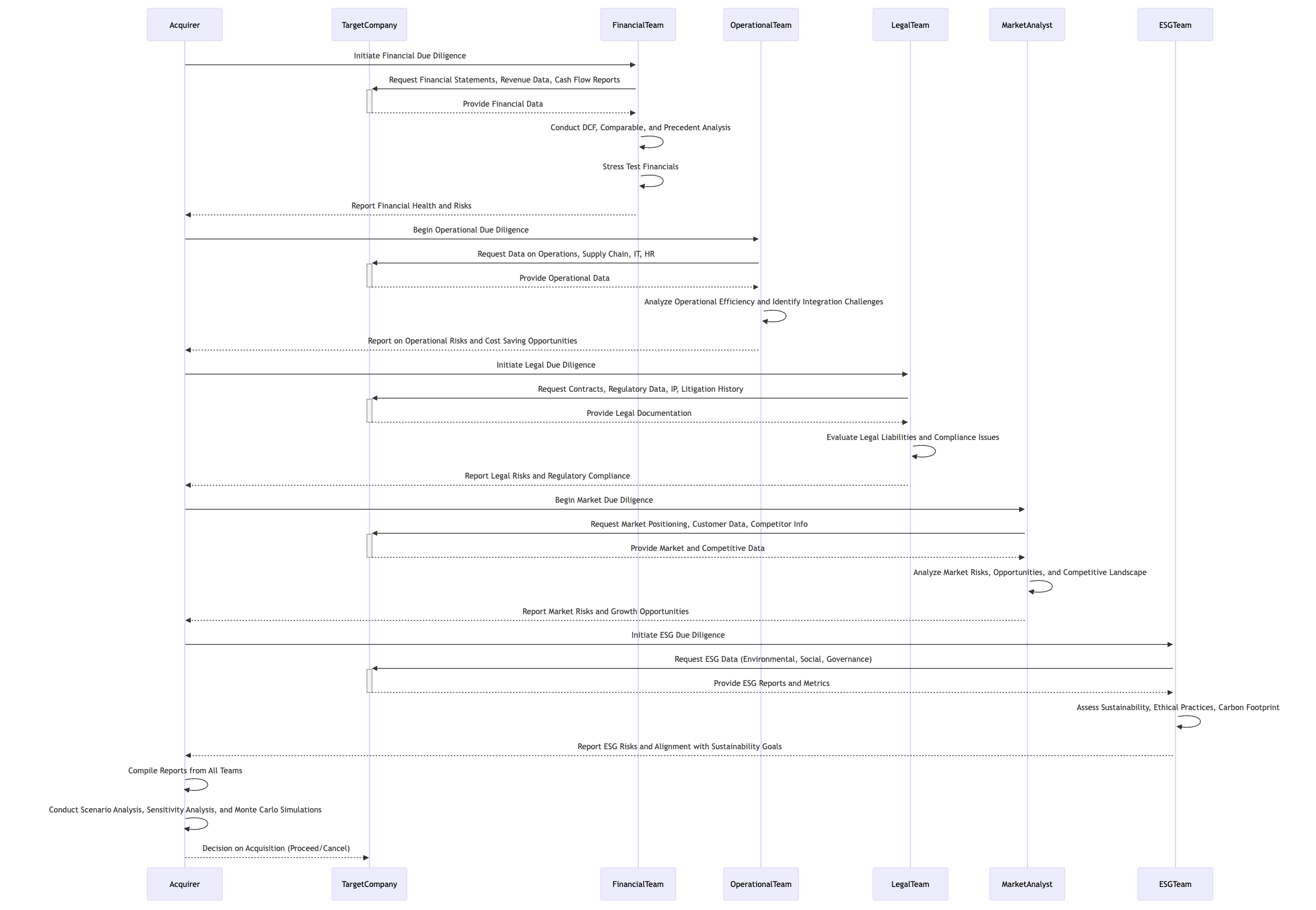

In practice, successful due diligence requires collaboration between cross-functional teams, including finance, legal, operations, human resources, and IT experts. This collaborative approach ensures that all aspects of the target’s business are thoroughly assessed, and potential risks are identified and addressed before the deal is finalized.

Figure 5.8: Sample business process of due diligence.

Due diligence is the bedrock of informed decision-making in M&A, offering a strategic, robust, and comprehensive evaluation of the target company. By integrating academic theories with industry best practices, companies can conduct due diligence that is both scientifically rigorous and practically relevant. This approach enables acquiring companies to uncover hidden risks, identify value-creating opportunities, and ensure that M&A transactions are aligned with their long-term growth and sustainability goals. Ultimately, a disciplined and thorough due diligence process is essential for transforming M&A transactions into successful, value-enhancing investments.

5.2. Comprehensive Due Diligence Scopes

Comprehensive due diligence in mergers and acquisitions (M&A) is a critical, multifaceted process that requires a strategic and scientific approach to ensure that all relevant risks and opportunities are identified, evaluated, and addressed. The complexity of modern business environments means that due diligence must encompass a broad spectrum of assessments—ranging from macro-level evaluations of market dynamics, competitive positioning, and regulatory environments to micro-level analyses of the target company's financial health, operational efficiency, and technological capabilities. A well-structured due diligence process ensures that the acquirer has a clear understanding of how the acquisition will affect its long-term growth, competitive advantage, and strategic positioning.

In today’s fast-evolving business landscape, academic and industry perspectives converge on the necessity of employing a multidisciplinary framework for due diligence, ensuring that the process is not limited to financial analysis but also covers legal, operational, environmental, and social dimensions. The expansion of the due diligence process, driven by the increasing relevance of enterprise risk management (ERM) frameworks and environmental, social, and governance (ESG) considerations, ensures a more robust and holistic analysis of the target company.

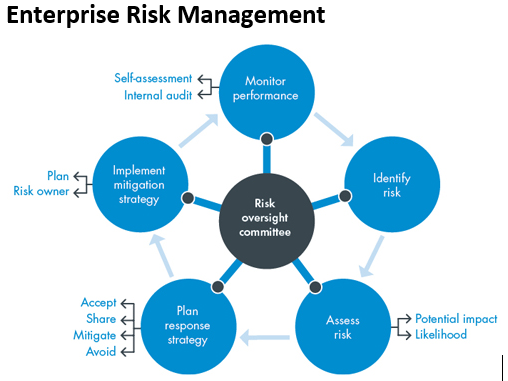

From an academic standpoint, due diligence can be closely tied to enterprise risk management (ERM) frameworks, which are designed to provide organizations with a structured approach to identifying, assessing, and mitigating risks across all functional areas of the business. These frameworks promote a holistic perspective on risk, ensuring that due diligence is comprehensive and systematic. ERM frameworks emphasize that risks are interconnected, meaning that financial risks may be influenced by operational or legal challenges, while reputational risks could stem from governance or ESG issues. By applying ERM principles, acquiring companies can identify potential threats that may not be immediately apparent through traditional financial analysis alone.

Figure 5.9: Main activities in ERM framework.

ERM frameworks also underscore the importance of scenario planning and stress testing, helping acquirers to understand how various risk factors might interact under different market conditions. For example, an acquirer might use ERM principles to assess how a target company’s financial performance could be affected by a supply chain disruption or regulatory change, enabling more informed decision-making.

The integration of ERM into the due diligence process ensures that risks are considered in a comprehensive manner, helping companies to avoid the narrow focus that can lead to significant post-acquisition pitfalls. ERM also emphasizes the need for risk mitigation strategies that can be implemented both during and after the acquisition to minimize negative impacts and maximize synergies.

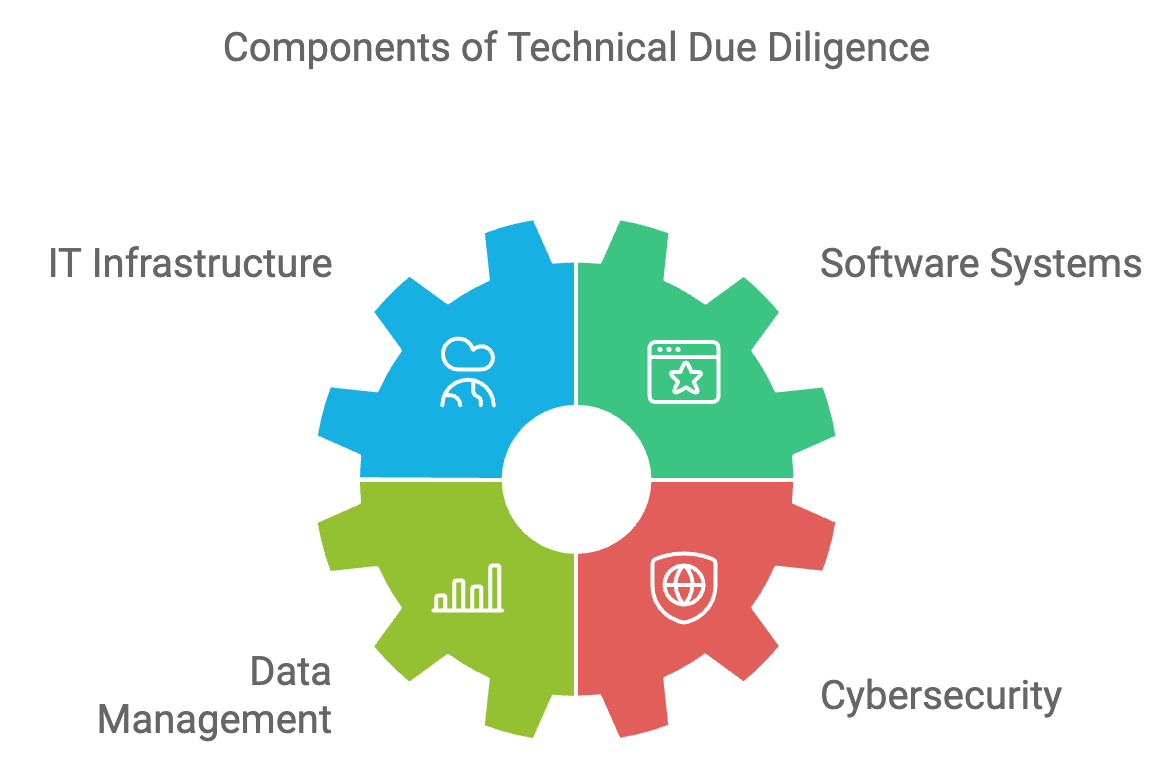

Another critical area of due diligence is assessing the target’s readiness for digital transformation. In today’s data-driven economy, the ability to leverage technology for operational efficiency, customer engagement, and innovation is a key driver of competitive advantage. Digital due diligence involves evaluating the target’s IT infrastructure, data management capabilities, cybersecurity measures, and digital business models to ensure that the company is well-positioned to adapt to technological disruptions.

For example, in an acquisition within the retail sector, digital due diligence might focus on assessing the target’s e-commerce platforms, data analytics capabilities, and omnichannel strategies. The acquirer would evaluate whether the target’s technology stack is scalable and compatible with its own systems, and whether the company has the digital capabilities to compete in a highly competitive, technology-driven market.

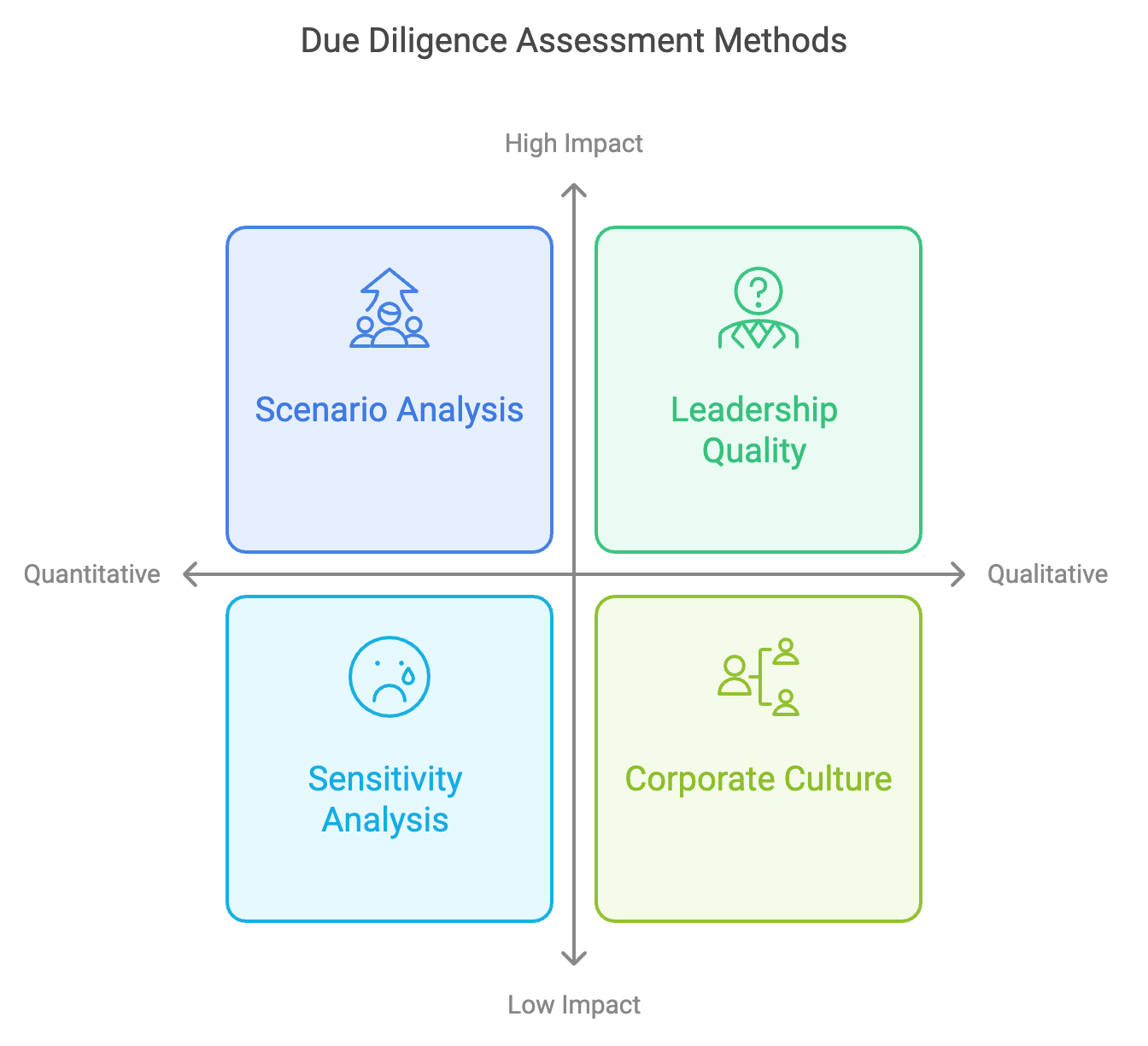

The due diligence process must be grounded in scientific and systematic methods to ensure thoroughness, objectivity, and accuracy. This means employing both quantitative and qualitative assessments to gain a complete understanding of the target company. Quantitative methods, such as scenario analysis, sensitivity analysis, and Monte Carlo simulations, allow acquirers to model potential risks and evaluate different outcomes based on variable factors such as market conditions, financial performance, and operational efficiency. These scientific methods help acquirers make data-driven decisions and avoid over-reliance on assumptions or overly optimistic projections.

Figure 5.10: The due diligence assessment methods.

Qualitative assessments are equally important, as they provide insights into the target’s leadership quality, corporate culture, brand reputation, and stakeholder relationships. These factors, while not easily quantifiable, can have a significant impact on the success of the acquisition. For example, a qualitative assessment of the target’s leadership team might reveal whether they have the vision and experience to navigate post-acquisition challenges, while an analysis of the company’s culture might highlight potential integration risks that could lead to employee turnover or operational disruption.

Comprehensive due diligence in M&A transactions requires a multidisciplinary, scientific, and systematic approach to uncover the full spectrum of risks and opportunities that could affect the acquisition’s success. By incorporating academic frameworks such as ERM and leveraging industry best practices, companies can ensure that their due diligence processes are thorough and objective, covering financial, legal, operational, market, ESG, and digital transformation dimensions. This holistic approach enables acquiring companies to anticipate challenges, capitalize on synergies, and align their acquisitions with long-term strategic and sustainability goals, thereby creating value that extends well beyond the transaction itself.

5.3. Business Due Diligence

Business due diligence is a critical component of the M&A process, designed to provide a comprehensive understanding of the target company’s core operations, business model, competitive positioning, and scalability. Unlike other forms of due diligence that focus on financials or legal matters, business due diligence dives into the operational heart of the company, examining the key drivers that sustain and grow its value. This makes it a cornerstone of strategic decision-making, helping acquiring companies determine not only the viability of the transaction but also its long-term contribution to growth and competitive advantage.

From an academic standpoint, business due diligence aligns closely with strategic management theories such as the resource-based view (RBV) and the dynamic capabilities framework. Both theories underscore the importance of assessing the target company’s internal resources and its ability to adapt to changing market conditions. Together, these frameworks provide a robust theoretical foundation for understanding the strategic fit between the acquirer and the target and for determining how the acquisition will enhance the acquirer’s overall value proposition.

The resource-based view (RBV) emphasizes the importance of acquiring resources that are valuable, rare, inimitable, and non-substitutable (VRIN). According to RBV, a company’s ability to sustain a competitive advantage lies in its unique resources—whether they be proprietary technologies, intellectual property, strong brand equity, or key customer relationships. Business due diligence, therefore, focuses on identifying whether the target company possesses these VRIN resources that can bolster the acquirer’s competitive position in the market.

For example, if an acquirer is looking to expand its product portfolio in the tech sector, business due diligence would closely assess whether the target possesses proprietary technology that is both difficult to replicate and highly valuable in the marketplace. Similarly, in industries such as pharmaceuticals, acquiring patents or specialized R&D capabilities would offer the acquirer a competitive edge. The RBV framework ensures that the due diligence process is not limited to financial metrics but extends to a deeper evaluation of the target’s strategic assets, which are essential for sustaining long-term growth.

In practice, industry leaders use RBV to evaluate acquisitions for their potential to enhance key competencies. For instance, Google’s acquisition of YouTube in 2006 was not just about acquiring a video-sharing platform; it was about gaining access to a massive user base and a highly scalable video distribution technology, which were rare and difficult to replicate at the time. This acquisition fit seamlessly into Google’s strategy of expanding its digital footprint and capitalizing on the rise of user-generated content—key VRIN resources that continue to drive Google’s competitive advantage.

While the RBV framework focuses on the acquisition of strategic resources, the dynamic capabilities framework goes a step further by emphasizing the importance of organizational flexibility and adaptability. This theory suggests that companies must continuously adapt, integrate, and reconfigure their internal and external capabilities to respond to rapidly changing environments. In the context of business due diligence, this means assessing whether the target company has the organizational agility required to thrive in evolving market conditions.

For instance, in industries where technological disruption or regulatory changes occur frequently, it is not enough for the target company to possess valuable resources—it must also be able to pivot and adapt to new opportunities and challenges. Business due diligence under the dynamic capabilities lens would evaluate the target’s ability to innovate, its culture of learning, and its track record of responding to market changes. This could include assessing the target’s R&D capabilities, its responsiveness to customer needs, or its ability to scale operations in response to market demand.

In industry practice, companies like Amazon have utilized dynamic capabilities in their acquisition strategies. Amazon’s purchase of Whole Foods was not just about acquiring a grocery chain; it was a strategic move that leveraged Amazon’s operational flexibility and technological prowess to innovate in the grocery sector. By integrating its e-commerce platform with Whole Foods’ physical stores, Amazon demonstrated its dynamic capability to reconfigure its resources to create new competitive advantages.

Figure 5.11: Best practices on due diligence process.

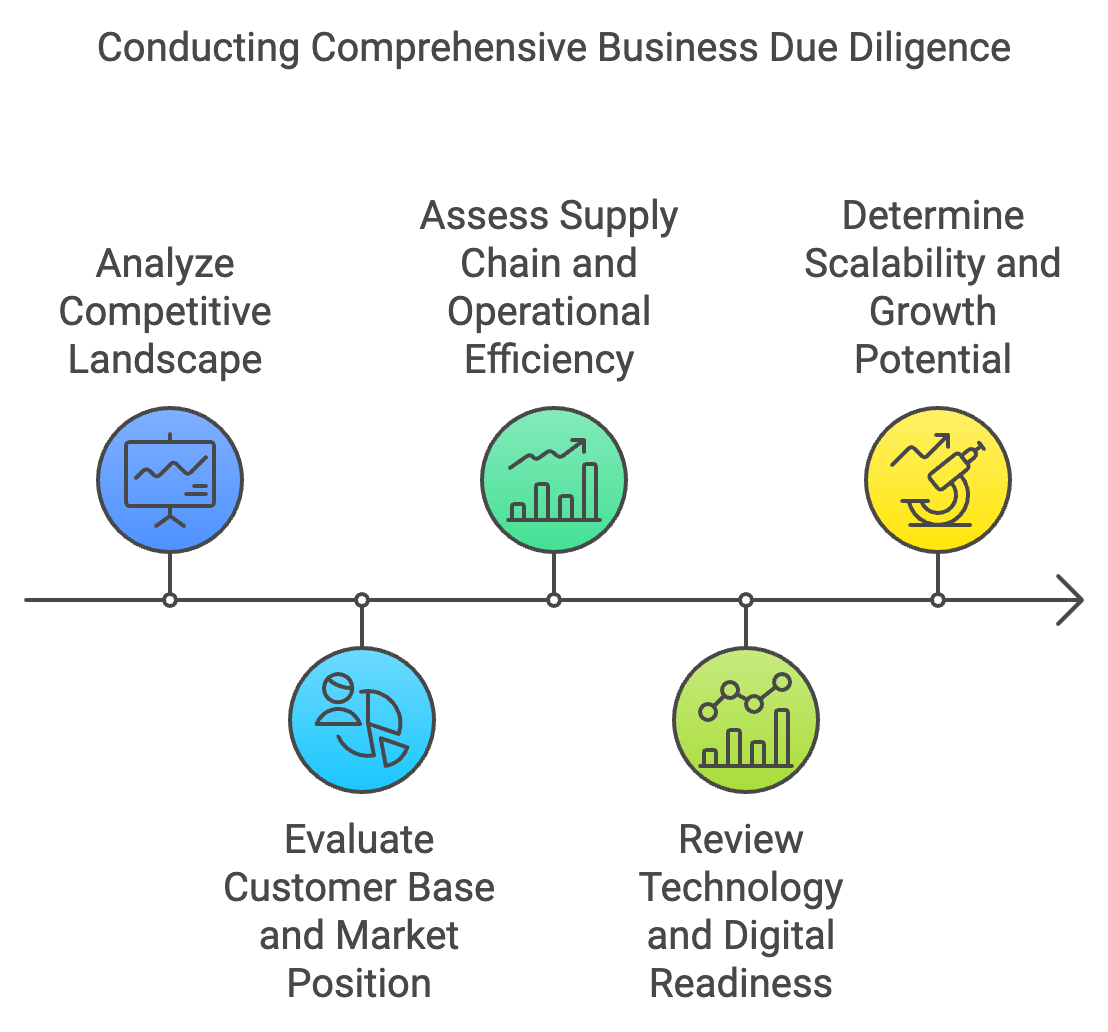

In the real world, business due diligence involves a detailed, data-driven analysis of several critical dimensions of the target company’s operations. Each of these components provides insights into how the acquisition will enhance the acquirer’s ability to compete, grow, and sustain long-term value.

Competitive Landscape A key component of business due diligence is analyzing the competitive landscape in which the target operates. This involves a deep dive into market positioning, identifying key competitors, evaluating the target’s market share, and assessing industry growth trends. By understanding the competitive forces that impact the target company, the acquirer can evaluate whether the target’s business model is sustainable and whether it has the potential to maintain or improve its position in the market post-acquisition. For example, a company looking to acquire a startup in the fintech space might evaluate how the target’s technology stacks up against competitors, whether its business model is scalable, and whether it has sufficient differentiation to defend against new market entrants.

Customer Base and Market Position A thorough analysis of the target’s customer base is essential for understanding the potential for growth and scalability. This involves segmenting the customer base, analyzing customer loyalty, and assessing the target’s ability to attract new customers in existing and new markets. Additionally, due diligence evaluates the target’s sales channels, pricing strategies, and revenue streams to determine if they are sustainable and aligned with market trends. In practice, this could involve assessing whether the target’s revenue is concentrated among a few key customers or if it has a diversified base that provides stability. Additionally, the acquirer might look at the target’s customer retention rates and brand equity to understand whether it has a competitive advantage in maintaining long-term customer relationships.

Supply Chain and Operational Efficiency The target’s operational efficiency, including its supply chain, production capabilities, and cost structures, is another critical area of focus. Business due diligence evaluates whether the target has the operational systems in place to scale efficiently post-acquisition. This might involve reviewing the target’s logistics network, supplier relationships, inventory management, and production processes. For instance, in the manufacturing sector, business due diligence would assess whether the target’s supply chain is robust enough to handle increased demand or whether there are inefficiencies that need to be addressed. A poorly integrated supply chain or outdated technology could pose significant risks to the acquirer’s ability to achieve cost savings or operational synergies.

Technology and Digital Readiness In today’s digital age, a target’s technology infrastructure and digital capabilities are critical factors in determining its long-term competitiveness. Business due diligence must assess whether the target’s technology is up-to-date, scalable, and compatible with the acquirer’s systems. Additionally, evaluating the target’s digital transformation efforts—such as its use of data analytics, artificial intelligence, or cloud computing—can provide insights into its innovation potential. For example, in a tech-driven acquisition, due diligence might involve a deep dive into the target’s software architecture, cybersecurity practices, and proprietary algorithms to ensure they align with the acquirer’s strategic goals and provide a platform for future growth.

Scalability and Growth Potential Ultimately, one of the primary goals of business due diligence is to assess the target’s scalability and growth potential. This involves evaluating how well the target can expand into new markets, increase production capacity, or introduce new products and services. Acquirers look for targets that have a proven business model that can be scaled up, with minimal risk of disruption or operational challenges. For instance, if a private equity firm is acquiring a fast-growing retail chain, due diligence would focus on understanding whether the target has the supply chain infrastructure, management capabilities, and financial resources to continue its expansion at the same pace. Business due diligence ensures that the acquirer is not overestimating the target’s growth potential and is prepared for the challenges that may arise during the scaling process.

Business due diligence is not just a qualitative process; it involves a high degree of scientific rigor and data-driven analysis. By leveraging market research, performance metrics, financial modeling, and competitive benchmarking, acquirers can make objective decisions about the strategic fit and growth potential of the target. This data-driven approach helps acquirers avoid the cognitive biases that often plague M&A decisions, such as over-optimism or the tendency to focus on short-term gains over long-term sustainability.

For example, financial models can be used to project future cash flows, while sensitivity analyses can test how the target’s business would perform under various market scenarios, such as a recession or a competitive pricing war. Data analytics tools can also be employed to analyze customer data, identify patterns, and predict future behavior, providing deeper insights into the target’s customer base and market positioning.

Business due diligence in M&A is a multidisciplinary, data-driven process that plays a crucial role in determining whether an acquisition will contribute to long-term strategic growth. By integrating academic frameworks such as the resource-based view and dynamic capabilities theory, acquiring companies can assess whether the target possesses the strategic resources and organizational flexibility needed to thrive in a competitive marketplace. In practice, business due diligence involves a detailed analysis of the target’s competitive landscape, operational efficiency, technology infrastructure, and growth potential, ensuring that the acquisition aligns with the acquirer’s long-term objectives. Through a combination of scientific rigor and strategic insight, business due diligence enables companies to make informed decisions that drive sustainable value creation in the M&A process.

5.4. Market Analysis and Competitive Landscape

Assessing a target company’s position within its industry and the broader competitive landscape is critical in determining its long-term growth prospects and potential value post-acquisition. This process goes beyond a superficial understanding of the company’s current market share and revenue, requiring a deep dive into macroeconomic trends, industry dynamics, technological shifts, and the competitive forces that shape the market. By conducting a thorough market analysis, acquirers can evaluate whether the target company is well-positioned to sustain its competitive edge and capitalize on growth opportunities or if it is vulnerable to competitive pressures that could erode its value.

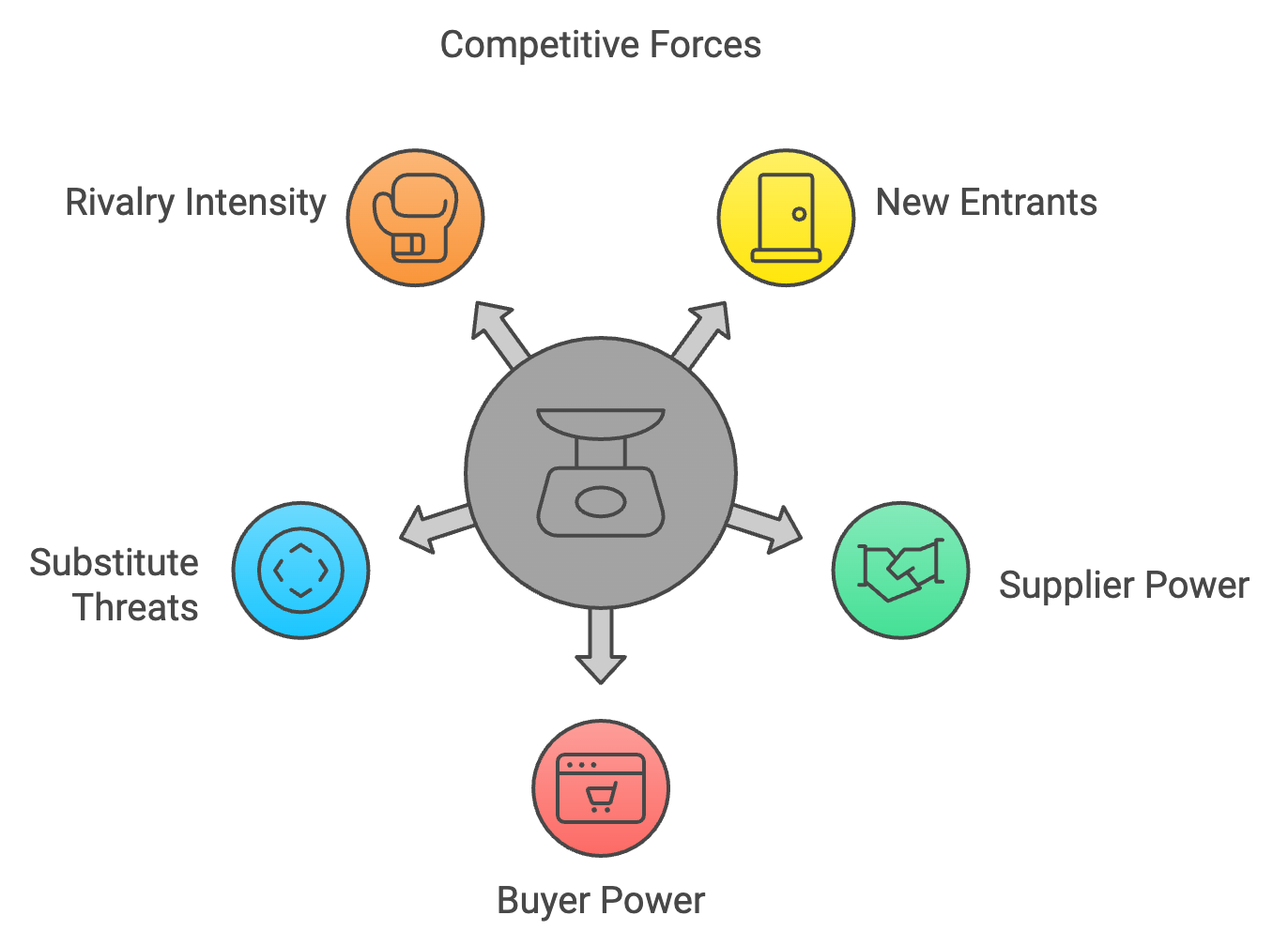

From an academic standpoint, Porter’s Five Forces framework remains one of the most widely recognized and robust models for assessing the competitive landscape. Developed by Michael Porter, this model provides a systematic approach to analyzing the external factors that influence industry competition and profitability. By evaluating the five key forces—threat of new entrants, bargaining power of suppliers, bargaining power of buyers, threat of substitute products or services, and the intensity of rivalry within the industry—acquirers can assess the target’s ability to generate sustainable profits and maintain a strong competitive position.

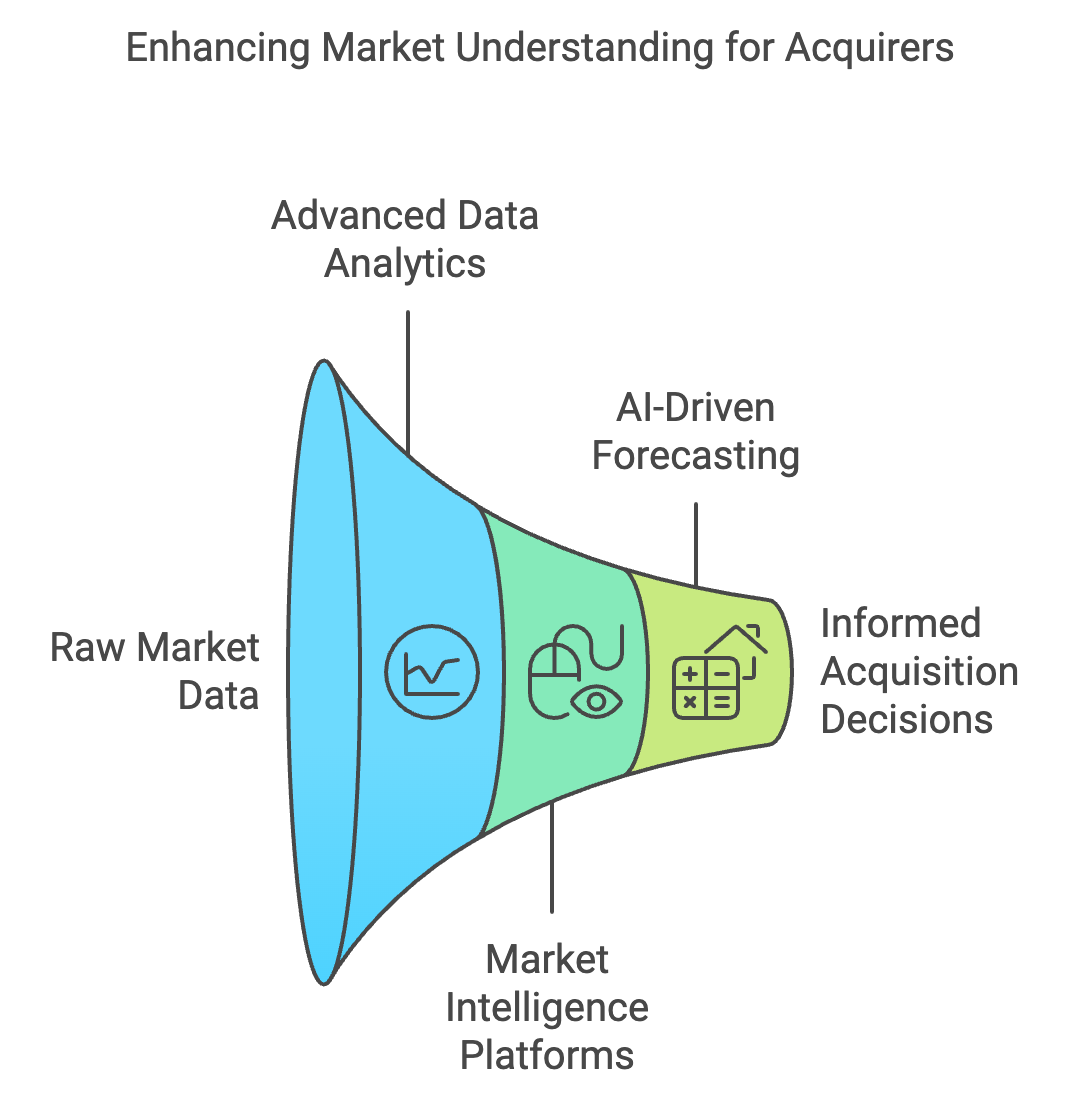

However, in today’s rapidly evolving markets, traditional frameworks must be supplemented with modern industry practices that leverage advanced technologies and data-driven insights. Industry practitioners use cutting-edge tools, such as data analytics platforms, market intelligence software, and artificial intelligence (AI)-driven forecasting, to gather real-time insights on customer behavior, competitor strategies, regulatory changes, and emerging market trends. By integrating both academic frameworks and modern industry practices, market analysis becomes a strategic, data-driven process that allows companies to make informed decisions about the target company’s growth potential, scalability, and alignment with broader industry trends.

Figure 5.12: Competitive forces on M&A based on Porter’s model.

Porter’s Five Forces model offers a robust academic framework for evaluating the competitive forces that shape an industry. Each of the five forces provides insights into the external pressures that may affect the target company’s profitability and long-term sustainability.

Threat of New Entrants: The ease with which new competitors can enter an industry plays a significant role in determining the competitive environment. High barriers to entry—such as capital requirements, economies of scale, access to distribution channels, or strong brand loyalty—help protect existing companies from new entrants. Conversely, low barriers to entry increase the risk of new competitors entering the market, driving down prices and eroding market share. In M&A due diligence, evaluating the threat of new entrants helps the acquirer assess the target company’s ability to defend its market position. For instance, in industries like pharmaceuticals, where regulatory approvals and R&D investments create high barriers to entry, established players enjoy a competitive advantage. However, in the tech industry, where innovation cycles are short and barriers to entry are relatively low, a target company’s market position may be more vulnerable to disruption from startups or competitors with breakthrough technologies.

Bargaining Power of Suppliers: Suppliers can exert significant influence on an industry, particularly when there are few alternatives or when they control critical inputs. If the target company is heavily dependent on a small number of suppliers, this can lead to increased costs, reduced profitability, and supply chain vulnerabilities. Alternatively, if the target has multiple suppliers or has vertically integrated supply chains, it may have more negotiating power and lower operational risk. Understanding the supply chain dynamics is crucial in market analysis. Acquirers must evaluate the target’s supplier relationships, dependencies, and the potential for supply chain disruptions that could affect cost structures and operational efficiency.

Bargaining Power of Buyers: The power of buyers—customers in this context—affects pricing, product development, and overall profitability. In markets where buyers have significant negotiating leverage, such as in highly commoditized industries, they can demand lower prices or higher-quality products, which can compress margins. Conversely, in markets with few buyers or differentiated products, companies can maintain pricing power and higher profitability. For instance, in industries like consumer electronics, where buyers have abundant alternatives and price sensitivity is high, the target company may face significant pressure to reduce prices or increase product features. A thorough analysis of the target’s customer base, buyer concentration, and customer loyalty is essential to understanding the risks and opportunities in maintaining revenue growth post-acquisition.

Threat of Substitutes: Substitutes pose a risk to companies by offering alternative solutions to customers that fulfill the same needs or functions. The threat of substitutes is particularly relevant in industries experiencing rapid technological advancement or shifting consumer preferences. If customers can easily switch to substitute products or services, the target company’s market share and profitability may be at risk. For example, in the energy industry, the rise of renewable energy sources such as solar and wind power presents a growing substitute threat to traditional fossil fuel companies. Similarly, in the media industry, the rise of streaming platforms like Netflix has disrupted traditional cable television providers. Acquirers need to assess the target company’s exposure to substitute products and its ability to innovate or differentiate its offerings to mitigate this risk.

Intensity of Rivalry: The level of competition among existing players in the industry determines how aggressively companies compete on price, product innovation, and customer acquisition. In highly competitive markets, profit margins are often squeezed, and companies must continuously innovate to stay ahead. Conversely, in industries with fewer competitors or strong brand loyalty, companies may enjoy a more favorable competitive environment. Analyzing the intensity of rivalry involves evaluating the number of competitors, the degree of differentiation among products, and the pace of innovation within the industry. This helps the acquirer understand whether the target company can maintain its competitive advantage or if it is likely to face sustained pressure from rivals.

While academic frameworks like Porter’s Five Forces provide valuable insights into the competitive landscape, modern industry practices rely heavily on data analytics and real-time market intelligence to supplement these traditional models. Companies today use sophisticated tools to analyze market trends, customer behavior, and competitive dynamics in much greater detail. These tools enable acquirers to gain granular insights into market positioning, forecast potential disruptions, and model various market scenarios.

Figure 5.13: Data analytic requirement in due diligence.

Advanced Data Analytics: Data analytics tools allow companies to process vast amounts of market and customer data to identify trends, preferences, and behavioral patterns. For example, acquirers can use machine learning algorithms to analyze historical sales data, customer purchase behavior, and pricing trends, helping them predict future demand and identify emerging market opportunities. Additionally, predictive analytics can be used to model different scenarios, such as how changes in customer preferences or economic conditions might impact the target company’s market share. This data-driven approach enables acquirers to make more informed decisions about the target company’s growth potential and scalability.

Market Intelligence Platforms: Market intelligence platforms offer real-time insights into competitor strategies, market developments, and regulatory changes. These tools aggregate data from various sources—such as industry reports, news articles, patents, and financial filings—allowing companies to track competitor activities and respond to market shifts proactively. For example, in industries such as pharmaceuticals or biotechnology, market intelligence platforms can provide insights into competitors’ clinical trials, new drug approvals, and patent filings, helping acquirers assess whether the target company is positioned to remain competitive in the face of innovation or regulatory changes.

AI-Driven Forecasting: Artificial intelligence (AI) and machine learning models are increasingly used to forecast market conditions and identify potential risks or opportunities. AI can analyze large datasets to detect patterns and correlations that may not be immediately obvious through traditional analysis methods. This allows acquirers to anticipate market shifts, technological disruptions, or changes in customer behavior that could impact the target company’s performance. AI-driven forecasting is particularly valuable in fast-moving industries like technology, where innovation cycles are short and market conditions can change rapidly. By leveraging AI, acquirers can improve the accuracy of their market forecasts and better understand the potential future trajectory of the target company’s industry.

In addition to competitive dynamics and customer trends, market analysis must also consider regulatory changes and environmental factors that could affect the target company’s market position. Increasingly stringent regulations—whether related to data privacy, environmental sustainability, or labor practices—can create significant risks or opportunities for companies.

For example, in the energy sector, regulatory shifts toward renewable energy mandates and carbon reduction targets can profoundly affect the long-term viability of companies that rely heavily on fossil fuels. Acquirers must assess the target company’s regulatory risk exposure and its readiness to adapt to new regulations. Similarly, environmental concerns, such as climate change and resource scarcity, are becoming key factors in evaluating market opportunities and risks, particularly in industries like agriculture, energy, and manufacturing.

Understanding the target company’s position within its industry and the broader competitive landscape is essential for assessing its long-term growth prospects. By integrating academic frameworks like Porter’s Five Forces with modern data-driven tools and industry practices, acquirers can conduct a comprehensive market analysis that goes beyond traditional methods. This holistic approach allows companies to evaluate the target’s competitive strengths, identify potential threats, and make informed decisions about scalability and growth potential. In an increasingly complex and dynamic market environment, the combination of rigorous academic models and cutting-edge technologies provides acquirers with a strategic advantage in making successful M&A decisions.

5.5. Customer Base and Supply Chain Assessment

A company’s customer base and supply chain are fundamental pillars influencing its operational performance, revenue stability, and long-term growth potential. Strategic due diligence in these areas enables acquirers to evaluate the target company's market dependencies, revenue drivers, and operational vulnerabilities with precision. This analysis is not only crucial for understanding the current state of the company but also for predicting future performance and identifying opportunities for value creation post-acquisition.

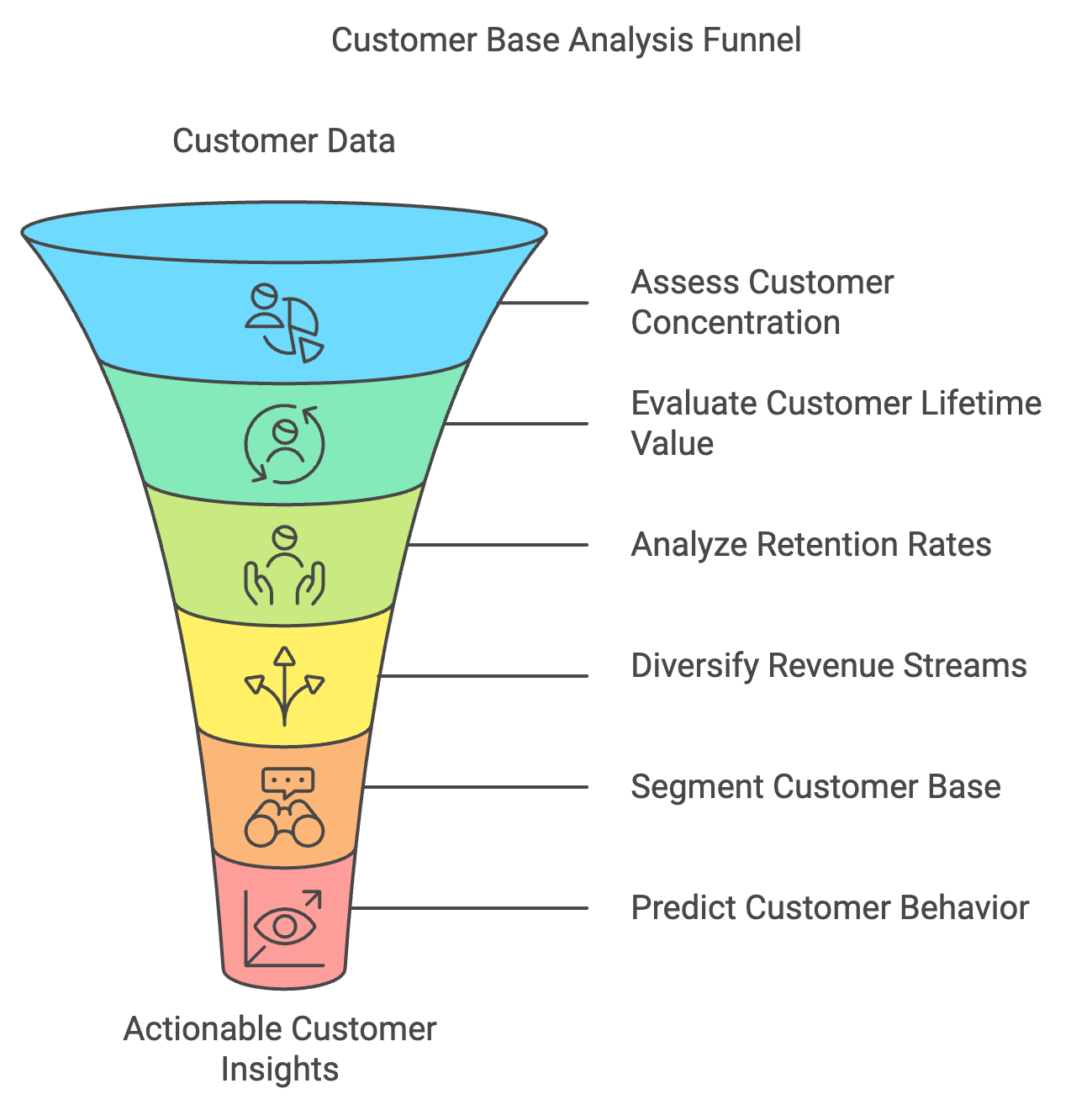

In academic literature, the analysis of a company’s customer base is deeply tied to the concept of customer concentration risk. This concept refers to the degree of risk associated with having a significant portion of revenue dependent on a small number of customers. High customer concentration exposes the company to revenue volatility, as the loss or reduction in spending by key clients could lead to substantial financial instability. Scholars have linked this risk to broader market performance, citing it as a factor that can influence the company’s valuation, competitive positioning, and ability to diversify.

From a strategic and operational standpoint, analyzing the customer base involves not only assessing customer concentration but also evaluating customer lifetime value (CLV), customer retention rates, and revenue diversification. These factors provide a comprehensive picture of the company's customer dynamics. In practice, customer segmentation models and predictive analytics are essential tools for acquirers, enabling them to identify patterns in customer behavior, assess loyalty, and estimate the likelihood of future revenue growth. Techniques such as cluster analysis, decision trees, and regression models are often employed to segment the customer base into actionable cohorts, allowing acquirers to assess which segments drive profitability, where customer churn might be high, and which segments offer the highest potential for upsell or cross-sell opportunities.

In academic research, the correlation between customer satisfaction and long-term revenue growth has been extensively studied. Models such as the Net Promoter Score (NPS) and Customer Satisfaction Index are commonly referenced frameworks that industry practitioners use to gauge customer loyalty and satisfaction. For acquirers, these metrics help determine not only the stability of the current customer base but also the likelihood of future customer acquisition and retention. Moreover, machine learning models that predict customer churn or next-best actions have become increasingly important in evaluating a company's ability to maintain and grow its customer relationships.

Figure 5.14: Customer-centric analysis in due diligence.

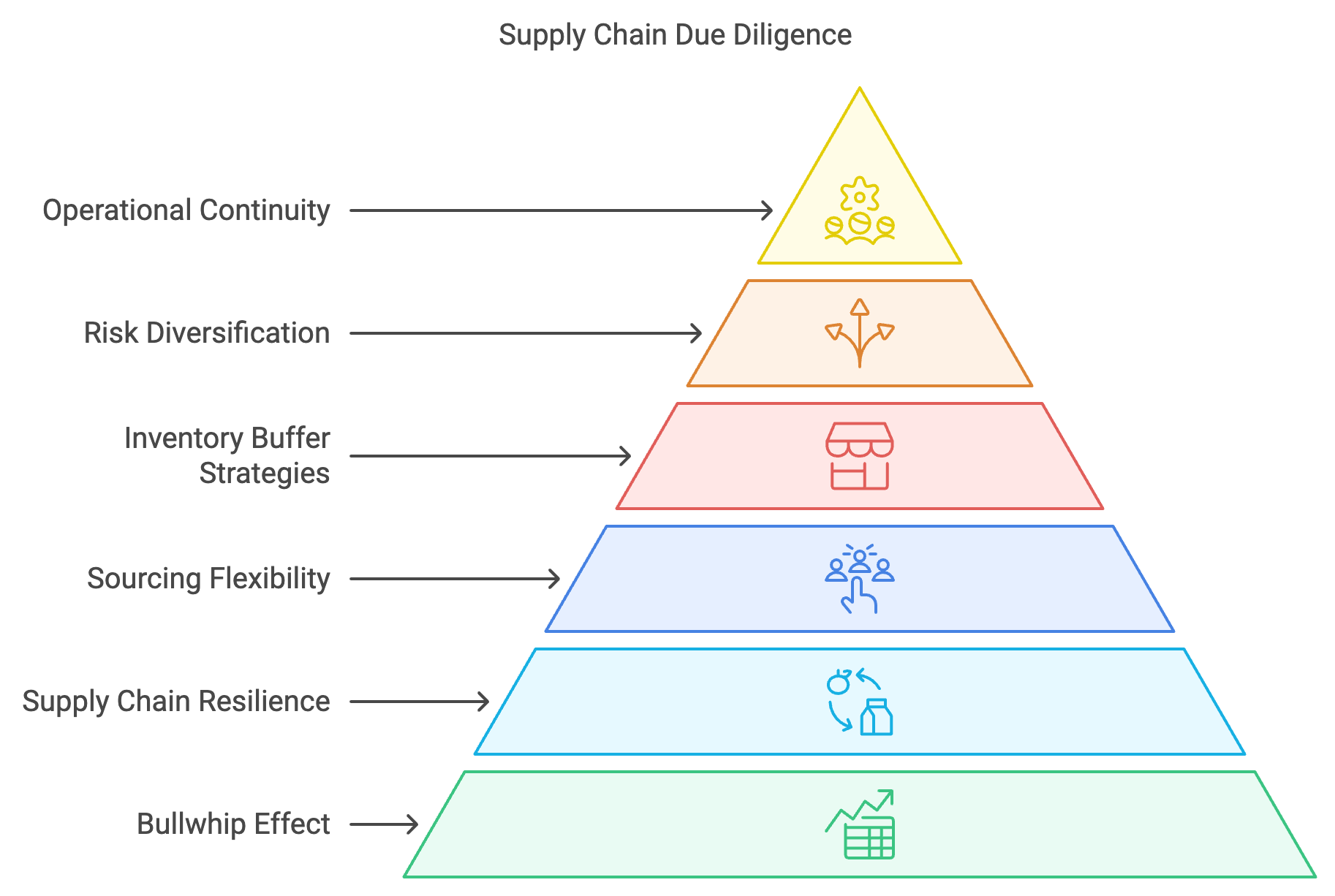

Supply chain assessment is another critical aspect of due diligence, as it directly impacts the company’s operational efficiency, scalability, and resilience. Academic frameworks such as the Bullwhip Effect and Supply Chain Resilience Theory provide structured methodologies to evaluate supply chain risks. The Bullwhip Effect describes the increasing variability in order quantities as they move up the supply chain, which can lead to inefficiencies in inventory management and production. Understanding how well a target company mitigates this effect is crucial for acquirers in industries where small fluctuations in demand can have outsized impacts on supply chain stability, such as manufacturing and retail.

Supply chain resilience is another key focus in academic literature. It refers to the ability of a supply chain to recover from disruptions and maintain operational continuity. This concept is particularly relevant in today's globalized economy, where supply chains are exposed to various risks, including geopolitical tensions, natural disasters, pandemics, and cyberattacks. Resilience is often measured by the flexibility of sourcing, inventory buffer strategies, and risk diversification across suppliers. An acquirer’s due diligence should evaluate the robustness of these strategies to ensure that the target company can withstand unforeseen shocks without compromising profitability.

Figure 5.15: Key aspects on supply chain due diligence.

From an industry perspective, supply chain due diligence involves a detailed examination of supplier relationships, procurement practices, inventory management, and logistics capabilities. Industry practitioners assess not only the company’s existing supplier contracts but also its reliance on single-source suppliers and exposure to market fluctuations in critical inputs. A comprehensive supply chain analysis also examines the target company’s logistical infrastructure—whether it has the capacity to scale operations efficiently or if it is vulnerable to bottlenecks that could hinder growth post-acquisition.

Moreover, modern supply chains are increasingly being evaluated through the lens of digital transformation. The integration of data analytics, blockchain for supply chain transparency, and IoT for real-time tracking are technologies that can significantly enhance supply chain visibility and resilience. Acquirers look for evidence of digitally-enabled supply chains as part of their due diligence, assessing whether the target company is leveraging these technologies to optimize operations and reduce risks.

Ultimately, a thorough and strategic due diligence process must integrate insights from both customer base analysis and supply chain assessment. By aligning academic theories with industry best practices, acquirers can form a holistic view of the target company’s operational health and potential risks. For example, understanding customer concentration risk helps acquirers predict revenue volatility, while supply chain resilience assessments help gauge operational continuity under stress. Both dimensions are critical for identifying opportunities for optimization and growth post-acquisition.

Strategically, acquirers can use these insights to create value post-acquisition through initiatives such as customer retention programs, supply chain optimization, and diversification strategies. By focusing on data-driven analysis and leveraging predictive models, they can also anticipate market changes and align the target company’s operations with future growth opportunities. This comprehensive approach ensures a more resilient, scalable, and profitable integration into the acquirer’s broader portfolio.

5.6. Financial Due Diligence

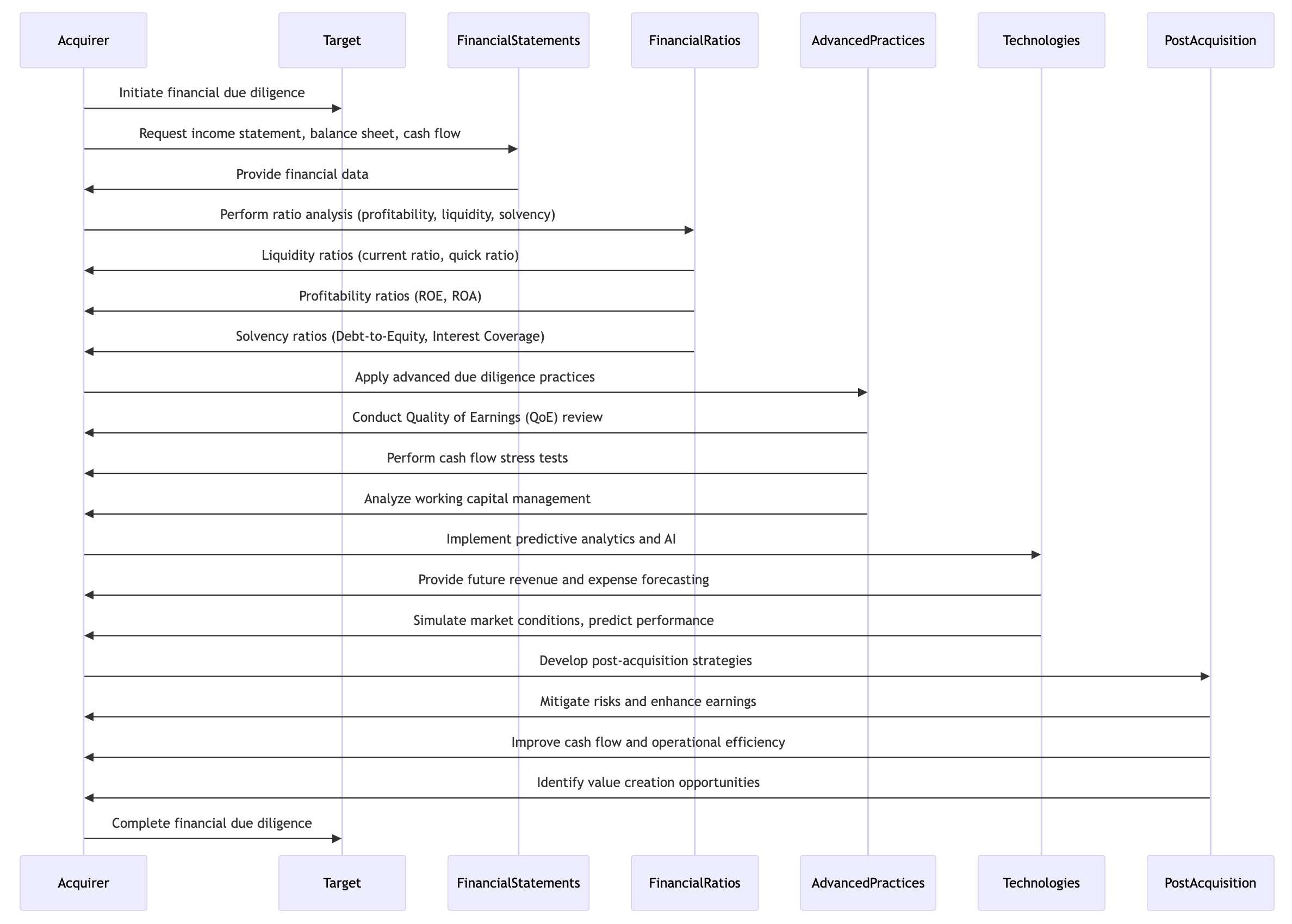

Financial due diligence is not merely a procedural step in the Mergers and Acquisitions (M&A) process—it is the cornerstone upon which acquirers build their understanding of a target company’s financial health, operational stability, and long-term growth potential. By providing a thorough evaluation of the target’s financial position, due diligence allows acquirers to assess the risks and opportunities that might influence the success of the acquisition. A comprehensive approach to financial due diligence goes beyond the surface-level review of financial statements and integrates academic principles with advanced industry practices, ensuring that every aspect of the target's financial performance is scrutinized and understood in depth.

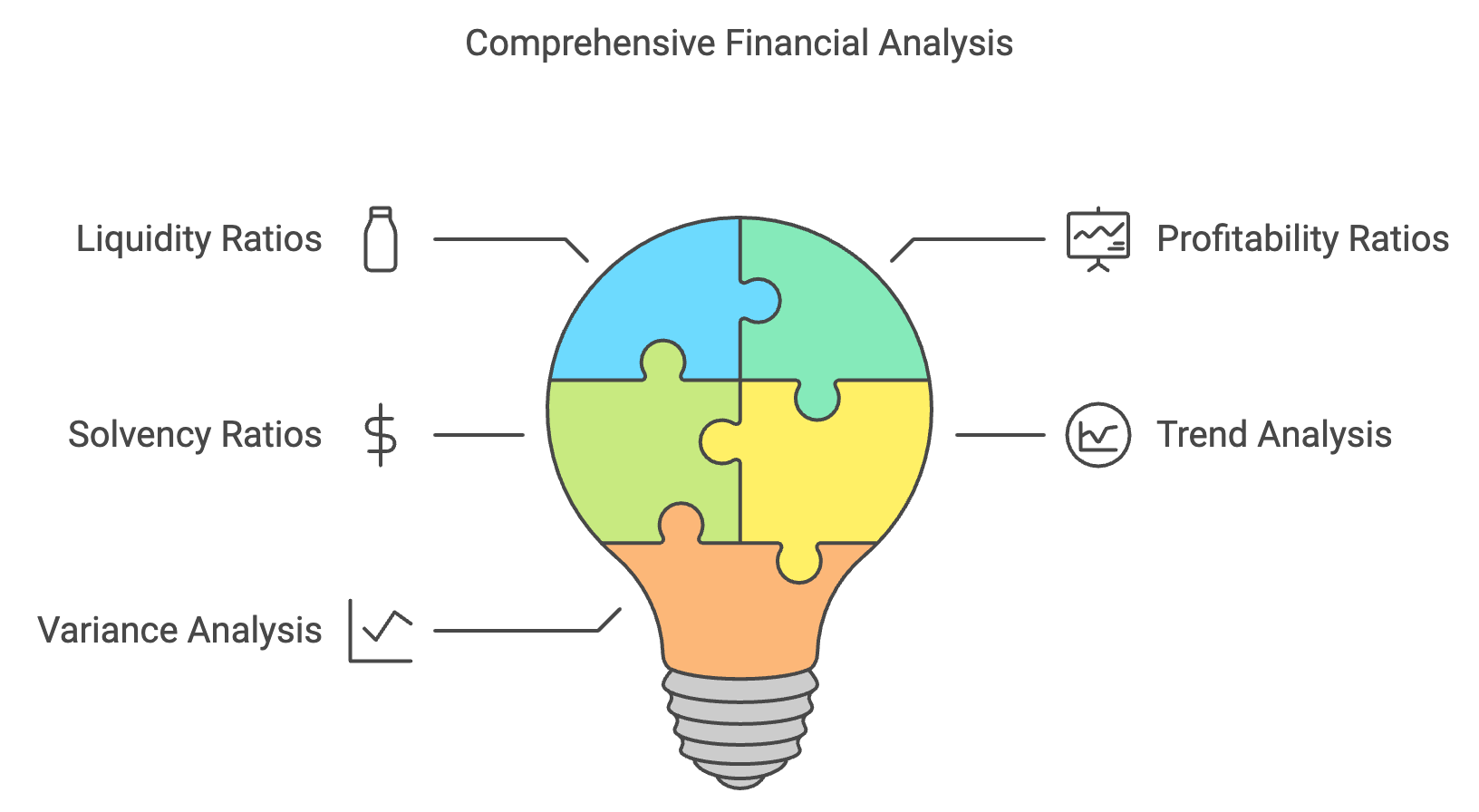

From an academic perspective, financial due diligence is guided by financial statement analysis theory, which focuses on the detailed examination of income statements, balance sheets, and cash flow statements. This approach is essential in evaluating key aspects of the target company’s operations, including profitability, liquidity, solvency, and working capital management. Academic literature provides frameworks for analyzing financial performance using tools such as ratio analysis, trend analysis, and variance analysis. These tools enable acquirers to evaluate the target company’s financial performance in a structured and consistent manner, providing insights into potential red flags or areas of concern.

Financial ratios play a central role in academic financial analysis. For instance, liquidity ratios such as the current ratio and quick ratio assess a company’s ability to meet its short-term obligations. These ratios are particularly important in evaluating a company's operational flexibility and short-term financial health. A company with weak liquidity may face challenges in sustaining operations, especially during market downturns or unexpected disruptions. Similarly, profitability ratios such as return on equity (ROE) and return on assets (ROA) are essential in assessing the company’s ability to generate profits from its resources. These ratios are widely regarded as indicators of management’s efficiency in deploying capital and assets to drive growth and returns. Additionally, solvency ratios like the debt-to-equity ratio and interest coverage ratio help acquirers understand the company’s long-term financial stability. High levels of debt or poor interest coverage can signal financial distress, which would raise concerns about the target’s ability to sustain operations and service its debt in the future.

Figure 5.16: Key aspects on finance due diligence.

In addition to ratio analysis, trend analysis allows acquirers to evaluate fluctuations in key financial metrics over time. By examining trends in revenue, operating expenses, and profit margins, acquirers can assess the target company’s financial stability and growth trajectory. Consistent trends in revenue growth and expense control are typically indicators of operational strength, while erratic fluctuations may suggest deeper issues such as market volatility, operational inefficiencies, or poor management. Variance analysis further complements this by providing a detailed breakdown of deviations in financial performance, helping acquirers identify potential areas where financial expectations have not been met.

While academic frameworks provide a foundation for analyzing financial statements, industry practitioners have developed more advanced techniques that allow for a deeper and more comprehensive assessment of a company’s financial position. One of the most critical components of industry due diligence is the Quality of Earnings (QoE) review. A QoE analysis goes beyond the numbers reported on financial statements and examines whether the company’s earnings are sustainable, recurring, and free from distortions caused by one-time events or aggressive accounting practices. This process distinguishes between core operational earnings and non-recurring income, such as gains from asset sales, tax benefits, or extraordinary items, which can inflate profitability artificially. By focusing on the quality and sustainability of earnings, acquirers can avoid overpaying for a company based on inflated or unsustainable earnings figures.

Another essential practice in industry due diligence is the use of cash flow stress tests. These tests simulate various economic scenarios, such as market downturns, interest rate hikes, or shifts in demand patterns, to assess the company’s ability to generate sufficient cash flow under adverse conditions. Cash flow is a critical component of a company’s financial health, as it determines the ability to meet operational and financial obligations, invest in growth, and withstand external shocks. By running stress tests, acquirers can gain insights into the target company’s financial resilience and determine whether it has built-in buffers to absorb potential shocks without compromising its operational continuity. This practice is particularly important in capital-intensive industries where liquidity and cash flow predictability are crucial to sustaining operations.

In addition to earnings quality and cash flow resilience, industry practitioners also place significant emphasis on working capital management during financial due diligence. Working capital is the lifeblood of any business, as it represents the short-term funds necessary to cover day-to-day operations. Poor working capital management can lead to liquidity constraints, operational bottlenecks, and ultimately financial distress. During due diligence, acquirers examine the target’s inventory turnover, accounts receivable, and accounts payable cycles to evaluate the efficiency of its working capital management. Companies with inefficient working capital cycles may face cash flow challenges, which could limit their ability to scale operations post-acquisition.

Furthermore, industry practitioners pay close attention to the working capital adjustment mechanism in M&A transactions. This mechanism ensures that the target company’s working capital levels are in line with normal operational requirements at the time of closing, protecting the acquirer from unforeseen liquidity shortfalls. By scrutinizing working capital levels and adjusting for any discrepancies, acquirers can ensure that they are not overpaying for a company that may experience operational disruptions due to liquidity constraints.

Beyond traditional financial analysis, the integration of modern technologies such as predictive analytics, artificial intelligence (AI), and machine learning is increasingly transforming the financial due diligence process. These technologies allow for more precise forecasting of future revenues, expenses, and cash flows, enhancing the accuracy of financial assessments. For instance, AI-driven models can simulate various market conditions and predict how a target company’s financial performance may evolve based on historical data, industry trends, and macroeconomic factors. This data-driven approach allows acquirers to make more informed decisions about the potential risks and opportunities associated with an acquisition.

The strategic implications of financial due diligence extend far beyond the immediate transactional analysis. By identifying risks such as unsustainable earnings, liquidity challenges, and inefficiencies in working capital management, acquirers can develop targeted post-acquisition strategies aimed at enhancing the financial performance of the target company. For instance, if due diligence reveals vulnerabilities in cash flow management, acquirers may implement strategies to improve liquidity through better working capital management or debt restructuring. Similarly, if earnings quality is found to be weak, acquirers can focus on strengthening core operational activities to stabilize profitability and drive long-term growth.

Figure 5.17: Sample business process for comprehensive due diligence.

In conclusion, financial due diligence is a multifaceted and strategic process that plays a critical role in the M&A landscape. By combining academic financial analysis frameworks with advanced industry practices, acquirers can gain a comprehensive understanding of a target company’s financial health and future potential. This integrated approach ensures that financial risks are identified and mitigated, while opportunities for value creation are fully explored. As the M&A landscape becomes increasingly competitive and complex, the ability to perform robust financial due diligence will continue to be a key differentiator for successful acquisitions, ensuring that acquirers make informed, data-driven decisions that align with their long-term strategic objectives.

5.7. Financial Statement Analysis

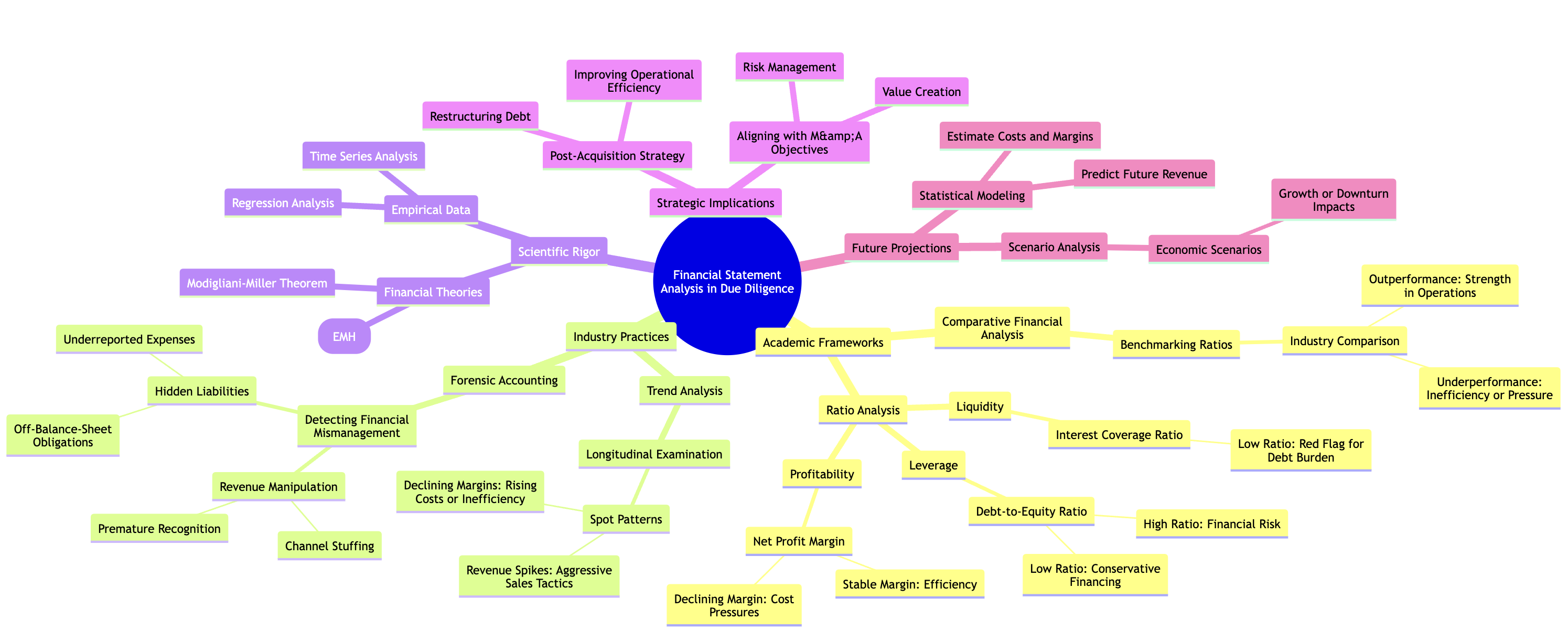

Financial statement analysis is a fundamental component of financial due diligence, providing a systematic and detailed examination of a target company’s historical financial performance, current financial health, and future projections. This process combines academic frameworks and industry best practices to create a comprehensive evaluation of the target's financial standing, offering acquirers key insights into the company’s operational efficiency, risk profile, and potential for growth. By integrating rigorous analysis methods with strategic interpretation, acquirers can make more informed decisions about whether an acquisition aligns with their financial goals and risk appetite.

Figure 5.18: Comprehensive scopes of financial statement analysis.

In academic literature, financial statement analysis is grounded in established theoretical frameworks such as ratio analysis and comparative financial analysis. These methods allow for a structured and consistent approach to assessing a company’s financial health. Ratio analysis, for example, uses key financial metrics to evaluate the target company’s leverage, liquidity, profitability, and efficiency. Common ratios such as the debt-to-equity ratio, interest coverage ratio, and net profit margin provide quantitative measures of the company’s financial stability.

The debt-to-equity ratio is used to assess the company’s leverage and financial risk by comparing the amount of debt it holds relative to its equity. A high debt-to-equity ratio may indicate that the company is overly reliant on debt financing, exposing it to higher interest costs and repayment risks. In contrast, a lower ratio suggests more conservative financing, which could indicate a stronger balance sheet and less exposure to financial distress.

The interest coverage ratio measures the company’s ability to meet its interest obligations from its earnings. This is a critical measure of financial health, particularly for companies with significant debt burdens. A low interest coverage ratio can be a red flag for acquirers, signaling that the company may struggle to cover its interest expenses, particularly in periods of declining revenue or rising interest rates.

Profitability ratios, such as the net profit margin, offer insights into the company’s operational efficiency by indicating how much profit it generates from its revenue. A declining net profit margin may raise concerns about rising operational costs, pricing pressures, or inefficiencies in the company’s cost structure. By analyzing these ratios over time, acquirers can detect trends that provide valuable information about the target’s financial performance and resilience in different market conditions.

Comparative financial analysis is another academic approach often used in due diligence. This method involves comparing the target company’s financial performance to industry peers or competitors. By benchmarking key financial ratios against industry averages, acquirers can assess whether the target company is underperforming or outperforming its competitors. For instance, a company with a lower-than-average profit margin may be less efficient in managing costs or face stronger competitive pressures, while a higher debt-to-equity ratio compared to peers may indicate higher financial risk.

While academic frameworks provide the foundational tools for financial statement analysis, industry practices add layers of practical rigor through techniques such as trend analysis and forensic accounting. Trend analysis involves examining financial statements over multiple reporting periods to identify patterns, anomalies, or shifts in the company’s financial metrics. This longitudinal approach helps acquirers spot red flags that may not be immediately apparent from a single reporting period.

For example, a sudden spike in revenue growth might indicate that the company has pursued aggressive sales tactics, such as offering significant discounts or extending payment terms to customers. While these practices can inflate short-term revenue, they may not be sustainable in the long term and could signal future cash flow problems or declining margins. Similarly, a consistent decline in profit margins over time may reflect rising operational costs, competitive pressures, or inefficiencies that could erode profitability post-acquisition.

Beyond trend analysis, forensic accounting techniques are often employed to detect potential signs of financial mismanagement or manipulation. This involves a deep dive into the financial statements to uncover issues such as revenue manipulation, hidden liabilities, or underreported expenses. Revenue manipulation can take the form of premature revenue recognition, where revenue is booked before it has been earned, or channel stuffing, where a company pushes excessive inventory onto distributors to inflate sales figures.

Similarly, hidden liabilities—such as off-balance-sheet obligations—can obscure the true extent of the company’s financial risk, while underreporting expenses can artificially inflate profit margins. Forensic accounting can reveal these hidden risks, providing acquirers with a more accurate assessment of the target company’s financial condition. This practice is particularly critical in industries with complex financial reporting or where the target company has a history of aggressive accounting practices.

The scientific rigor of financial statement analysis stems from its reliance on empirical data, statistical methods, and well-established financial theories. By applying these techniques, acquirers are not merely relying on subjective interpretations of the target company’s financial performance—they are utilizing quantitative data to form evidence-based conclusions about the company’s financial health.

For example, using statistical methods such as regression analysis or time series analysis, acquirers can model future financial performance based on historical data. These models can help estimate how key financial metrics—such as revenue, costs, and margins—will evolve under different economic scenarios, providing valuable insights into the target company’s potential future profitability and risks.

Additionally, the application of financial theories such as the Efficient Market Hypothesis (EMH) and Modigliani-Miller theorem can inform how acquirers assess the impact of capital structure on the target company’s valuation. For instance, under the Modigliani-Miller theorem, the value of a company is unaffected by its capital structure in perfect markets. However, in real-world scenarios with taxes, bankruptcy costs, and agency costs, the company’s leverage can significantly affect its risk profile and valuation, a consideration acquirers must weigh when evaluating the target’s debt levels.

By grounding financial statement analysis in these scientific principles, acquirers are better equipped to understand the nuances of the target company’s financial health, the potential risks it faces, and the opportunities for value creation post-acquisition.

The strategic implications of financial statement analysis go beyond simply evaluating historical performance. For acquirers, this process is critical in shaping post-acquisition strategies, identifying synergies, and managing risks. For example, if financial analysis reveals declining margins, acquirers can focus on operational efficiencies to improve cost structures post-acquisition. Similarly, if the analysis uncovers high leverage, the acquirer may prioritize debt restructuring or refinancing as part of their integration strategy.

A comprehensive financial analysis also helps acquirers understand whether the target’s financial metrics align with their strategic objectives. For instance, a company with a strong cash flow position and low leverage may be better suited for growth through additional investment, while a company with weaker liquidity and high debt may require a more conservative approach post-acquisition.

By integrating academic financial analysis frameworks with industry best practices, acquirers can ensure that their financial due diligence process is both rigorous and strategically aligned with their broader M&A objectives. This holistic approach enables acquirers to make informed, data-driven decisions, ensuring that they fully understand the risks and opportunities associated with the acquisition.

Financial statement analysis is not just about assessing past performance—it is a forward-looking process that integrates academic rigor with industry expertise to provide a comprehensive evaluation of a target company’s financial health. By leveraging ratio analysis, trend analysis, and forensic accounting, acquirers can uncover hidden risks and opportunities, while statistical modeling and financial theory provide a framework for projecting future performance.

Ultimately, a robust financial statement analysis process allows acquirers to make informed decisions, mitigate financial risks, and develop strategies for post-acquisition success. This integration of academic and industry approaches ensures that financial due diligence is thorough, strategic, and aligned with long-term objectives in the complex M&A landscape.

5.8. Valuation Techniques and Pricing Strategies

Valuation is a cornerstone of the Mergers and Acquisitions (M&A) process, representing a critical juncture where financial theory meets practical decision-making. The valuation determines not only the price the acquirer is willing to pay but also the success of the deal in generating long-term value. Given the complexity and strategic importance of this step, a robust and comprehensive valuation approach requires integrating academic frameworks with industry best practices, while adapting methods to the specific context of the acquisition.

Figure 5.19: Comparison of common valuation methods.

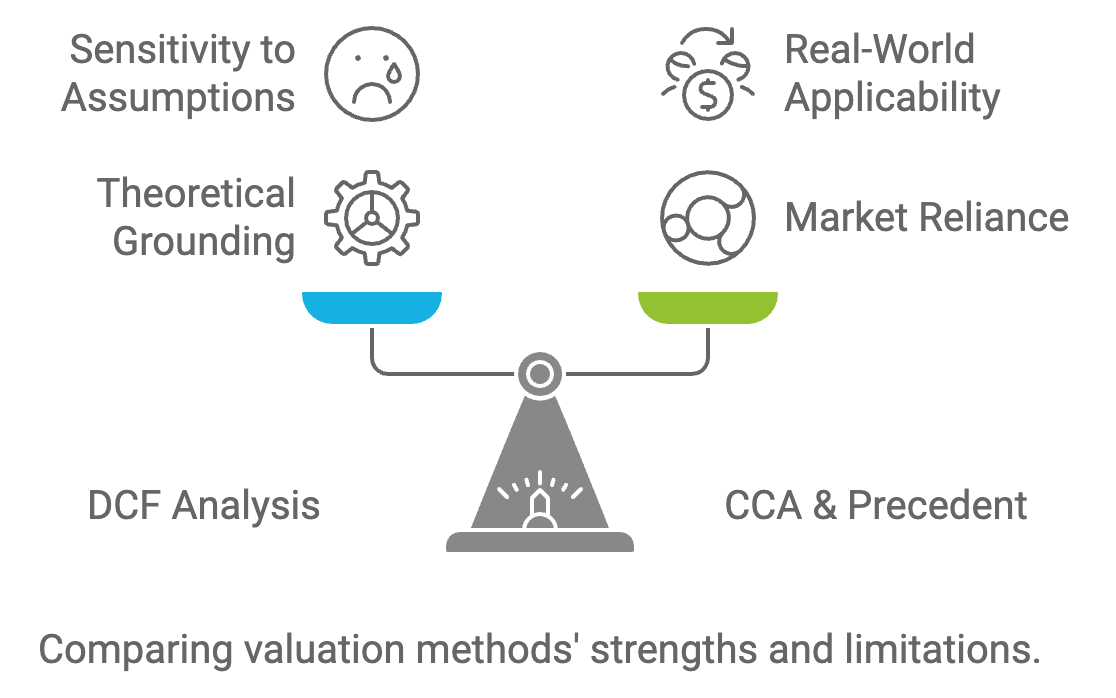

Several academic frameworks form the backbone of valuation techniques, each offering distinct insights into the target company’s worth. Among the most widely used are Discounted Cash Flow (DCF) analysis, Comparable Company Analysis (CCA), and Precedent Transaction Analysis. These methods help acquirers triangulate a fair and accurate valuation by considering various aspects of the target’s financial health and market positioning.

Discounted Cash Flow (DCF) analysis is grounded in financial theory, which asserts that the value of an asset is equivalent to the present value of its future cash flows, adjusted for time and risk. In essence, the DCF method calculates the value of a company based on its projected ability to generate future cash flows, which are then discounted to their present value using an appropriate discount rate (typically the weighted average cost of capital (WACC)). This discount rate reflects the risk associated with the company and its industry. In academia, the DCF method is considered a gold standard for valuing companies with stable and predictable cash flows because it provides a forward-looking and intrinsic view of a company’s earning potential. The method requires a detailed forecast of the company’s revenue, operating costs, and capital expenditures, all of which are used to project free cash flows (FCF). While DCF is highly regarded for its rigorous approach, it is also sensitive to assumptions regarding growth rates and discount rates. Thus, sensitivity analysis is often applied to test the robustness of the valuation under different scenarios, ensuring that the target’s value is not overestimated or underestimated due to overly optimistic or conservative assumptions.

Comparable Company Analysis (CCA), also referred to as the "market approach," involves comparing the target’s financial metrics with those of similar publicly traded companies in the same industry. Metrics like earnings before interest, taxes, depreciation, and amortization (EBITDA), price-to-earnings (P/E) ratios, and enterprise value (EV) multiples provide market-based benchmarks for valuation. In industry practice, CCA is particularly useful when there is a lack of visibility into the target’s future cash flows or when market comparables offer a reliable gauge of investor sentiment. CCA enables acquirers to derive a relative valuation by identifying how investors price similar companies, making it a market-driven approach. However, academic research also cautions against relying solely on CCA, as market valuations can fluctuate due to short-term trends or investor overreactions. Therefore, it is often used alongside other methods to avoid over-reliance on market sentiment.

Precedent Transaction Analysis offers another perspective, focusing on the valuation multiples derived from recent M&A deals involving companies similar to the target. By examining valuation multiples, such as EV/EBITDA or EV/Revenue from past transactions, acquirers can assess the price premiums paid in similar deals. This analysis provides a real-world gauge of how much companies in the same sector have fetched in the context of strategic acquisitions, which often include premiums for control and anticipated synergies. The academic merit of precedent transaction analysis lies in its reflection of actual deal-making behavior, capturing industry-specific dynamics and negotiation outcomes. However, industry professionals often stress that this method can be influenced by unique factors specific to past deals, such as synergies or special circumstances, that may not apply to the current transaction. As a result, while precedent analysis is a valuable tool, it is best used in conjunction with other valuation frameworks.

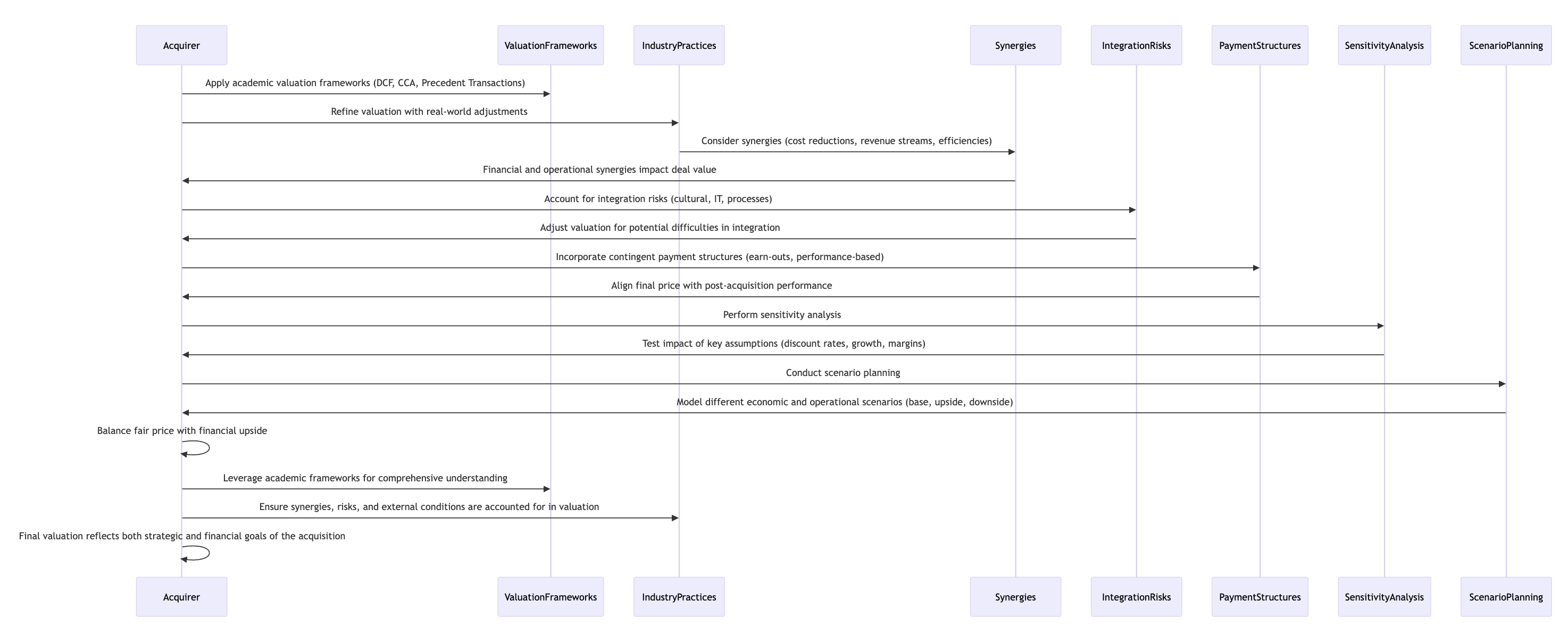

In practice, acquirers must adapt and refine these academic valuation frameworks to account for deal-specific conditions. Industry practitioners incorporate several real-world adjustments to valuation methods to ensure they accurately reflect the complexities of M&A transactions.

Figure 5.20: Sample business process of valuation method.

One of the most important adjustments in M&A valuation is the consideration of synergies. These are the additional value drivers that result from combining the operations of the acquirer and target, such as cost reductions, enhanced revenue streams, or operational efficiencies. Financial synergies (e.g., lower borrowing costs due to improved credit ratings) and operational synergies (e.g., economies of scale or cross-selling opportunities) can significantly impact the overall value of the deal.

At the same time, industry practitioners must also account for integration risks. Combining two companies often presents significant challenges, such as cultural clashes, integration of IT systems, or misaligned business processes. These risks can erode the potential value of the synergies that were factored into the valuation. Therefore, a comprehensive valuation should discount for potential integration difficulties, ensuring the deal’s financial upside is realistic.

Given the inherent uncertainties in valuation, especially for high-growth or volatile companies, acquirers often use contingent payment structures such as earn-outs or performance-based payments. An earn-out is a mechanism that ties a portion of the purchase price to the future performance of the target, ensuring that the acquirer does not overpay if the target fails to meet certain financial milestones post-acquisition. This structure mitigates valuation risks by aligning the final purchase price with the actual value delivered by the target after the acquisition.

Contingent payment structures are particularly useful when the target operates in a high-growth or uncertain industry, where future performance is difficult to predict. By incorporating earn-outs, acquirers can bridge valuation gaps and ensure that the deal price reflects actual post-deal outcomes rather than relying solely on projections.

Valuation is both an art and a science, requiring a multi-faceted approach that integrates quantitative financial models with strategic judgment. By combining academic frameworks with industry best practices, acquirers can arrive at a more accurate and nuanced valuation that reflects the complexities of the deal.

One of the key elements of a scientific approach to valuation is the application of sensitivity analysis and scenario planning. Sensitivity analysis tests the impact of changes in key assumptions—such as discount rates, growth projections, or EBITDA margins—on the overall valuation. This ensures that the valuation is robust and not overly dependent on any single assumption.

Scenario analysis goes a step further by modeling different economic or operational scenarios (e.g., base case, upside case, and downside case) to understand how the target’s value might fluctuate under various conditions. This allows acquirers to assess the risks and opportunities that could arise under different market conditions, providing a more comprehensive and strategic view of the deal.

A well-executed valuation process enables acquirers to strike a balance between paying a fair price and maximizing the financial upside of the deal. This involves not only calculating the intrinsic value of the target but also considering how the acquisition will align with the acquirer’s broader strategic objectives. For example, if the deal creates significant synergies or enables the acquirer to enter a new market, the valuation should reflect these additional value drivers.

Additionally, the acquirer must consider external market conditions—such as interest rates, inflation, and industry trends—which can significantly impact the target’s future performance and, by extension, its valuation. A valuation that fails to account for these external factors may result in overpayment or underpayment for the target.

Valuation in the M&A process is not just a technical exercise; it is a strategic decision-making tool that combines academic rigor with industry adaptation. By leveraging academic frameworks like DCF, CCA, and precedent transaction analysis, acquirers can gain a comprehensive understanding of the target’s intrinsic and market-based value. However, real-world adjustments for synergies, integration risks, and contingent payments ensure that the valuation reflects the complexities and uncertainties of the deal.

By adopting a scientific and multi-faceted approach, acquirers can arrive at a fair valuation that not only protects against downside risks but also maximizes the financial upside of the transaction. This balance is crucial in ensuring that the acquisition delivers long-term value and aligns with the acquirer’s broader strategic goals.

5.9. Legal and Regulatory Due Diligence

Legal and regulatory due diligence is a critical component of the Mergers and Acquisitions (M&A) process, as it provides a structured and thorough evaluation of the target company’s legal and regulatory risks. The success of any M&A transaction relies heavily on identifying, understanding, and mitigating these risks to avoid post-acquisition liabilities that could erode the value of the deal. A strategic, robust, and comprehensive approach to legal and regulatory due diligence requires integrating both academic theories and industry practices, ensuring that potential risks are evaluated from multiple perspectives and adequately addressed before the deal is finalized.

In academic literature, legal due diligence is closely tied to corporate governance theory, which underscores the importance of transparency, accountability, and compliance in managing legal risks. Corporate governance theory suggests that companies with strong governance frameworks are more likely to maintain compliance with laws and regulations, thereby reducing the risk of legal liabilities. From this perspective, legal due diligence serves not only as a mechanism to identify potential legal issues but also as a way to assess the overall governance structure of the target company. This includes examining the target’s decision-making processes, board structure, and ethical standards, all of which influence how effectively the company manages its legal and regulatory obligations.

One of the core tenets of corporate governance theory is transparency, which is essential for identifying legal risks in an acquisition. A well-governed company is more likely to maintain clear and accessible records of its contracts, regulatory filings, and litigation history, enabling the acquirer to conduct a more efficient and effective due diligence process. Additionally, accountability ensures that the target’s leadership is held responsible for maintaining compliance with laws and regulations, reducing the risk of legal issues arising post-acquisition.

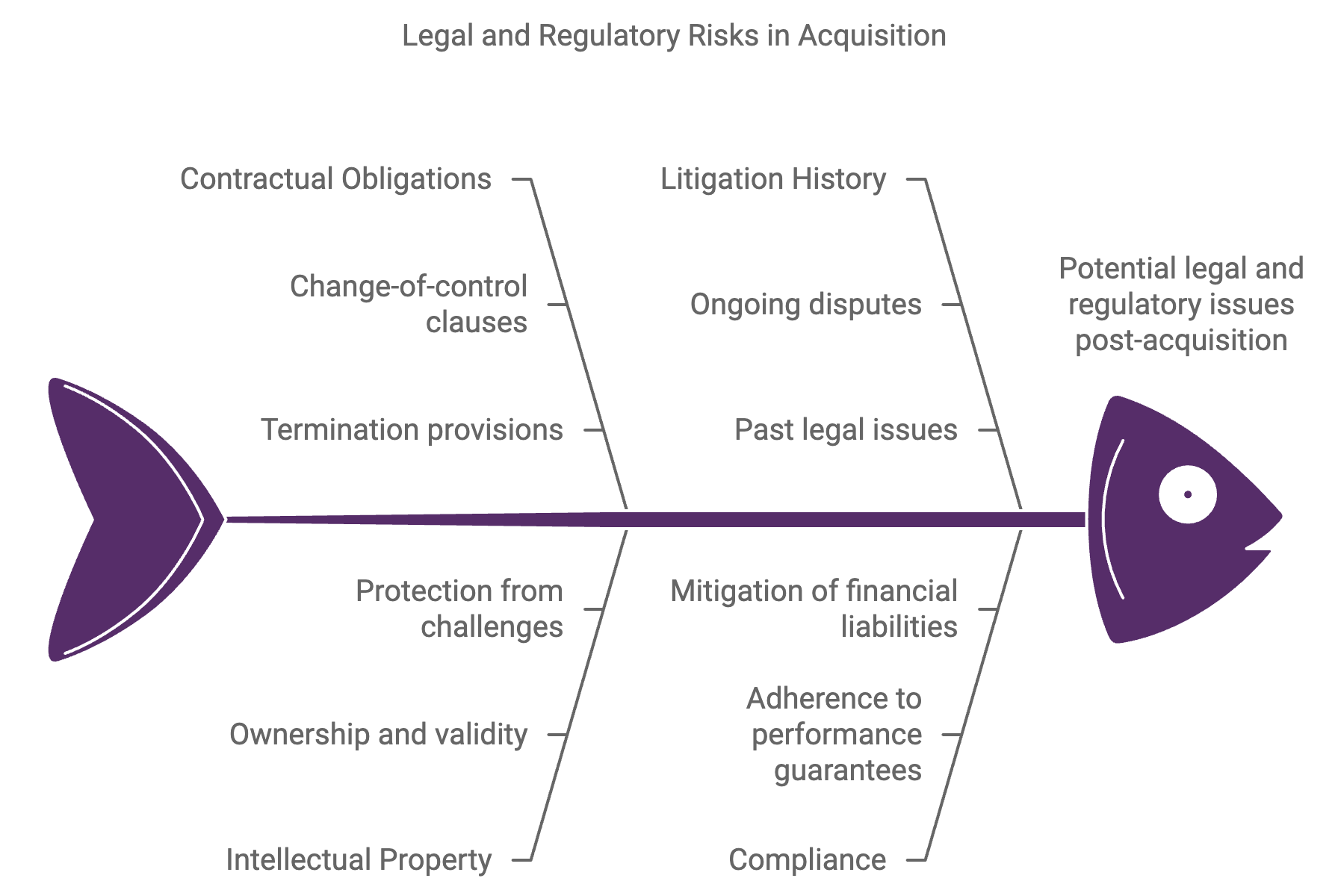

Figure 5.21: Legal and Regulatory Risks in Acquisition

In industry practice, legal and regulatory due diligence is a comprehensive process involving the review of multiple aspects of the target company’s legal framework. The key components include:

Contract review is one of the most critical aspects of legal due diligence, as it helps the acquirer understand the target’s existing contractual relationships and obligations. Contracts with customers, suppliers, employees, and partners can significantly impact the continuity of business operations post-acquisition. Particular attention should be paid to change-of-control clauses, termination provisions, and performance guarantees.

Change-of-control clauses can grant customers or partners the right to terminate agreements if ownership of the target company changes, potentially leading to the loss of key contracts or suppliers. For example, in industries with long-term supplier agreements or exclusive partnerships, losing these contracts can undermine the acquirer’s strategic goals. Similarly, termination provisions may trigger financial penalties or disrupt operations if contracts are terminated before their completion.

In addition to these considerations, the acquirer should evaluate the target’s compliance with performance guarantees and other contractual obligations. Failure to meet contractual standards could expose the acquirer to litigation or financial liabilities post-acquisition, making a thorough contract review essential to mitigating these risks.